For Non-Resident Indians (NRIs) who wish to invest in the Indian stock market, understanding the Portfolio Investment Scheme (PIS) is important. A PIS account helps NRIs invest in Indian shares while complying with regulations set by the Reserve Bank of India (RBI).

What is a PIS Account?

A Portfolio Investment Scheme (PIS) account is a special bank account that allows NRIs to buy and sell shares of Indian companies on recognized stock exchanges in India. The account enables banks to report NRI stock transactions to the RBI as required under Indian regulations.

PIS accounts are generally linked to:

- An NRE (Non-Resident External) savings account for repatriable investments.

- A trading account for buying and selling shares.

- A Demat account for holding shares electronically.

Why is a PIS Account Needed?

Traditionally, NRIs investing in Indian equities on a repatriable basis through an NRE account required a PIS account because:

1. Regulatory Compliance

- It helps track NRI investments and ensures compliance with RBI guidelines.

2. Transaction Reporting

- The designated bank reports stock market transactions to regulatory authorities.

3. Repatriation of Funds

- Investments made through an NRE-PIS route allow eligible sale proceeds and capital to be repatriated abroad, subject to applicable regulations.

4. Seamless Investment Process

- It links banking, trading, and demat services for efficient stock market investing.

Documents Required

Typically, banks and brokers may ask for:

- Passport copy

- Visa or residence permit

- Overseas address proof

- PAN card

- Passport-size photographs

- NRE bank account details

- FATCA/CRS declarations

- KYC documents

Requirements may vary between institutions.

How to Open a PIS Account

Step 1: Open an NRE Account

Choose an Indian bank that offers NRI banking services and open an NRE savings account.

Step 2: Apply for a PIS Account

Submit the required forms and documents to the bank. The bank will process the application and provide the PIS facility if applicable.

Step 3: Open an NRI Demat Account

Open an NRI Demat account with a depository participant or broker.

Step 4: Open an NRI Trading Account

Open a trading account with a broker that supports NRI investments.

Step 5: Link All Accounts

Link your NRE/PIS account, trading account, and Demat account to begin investing.

Key Rules to Keep in Mind

- One Bank Rule: You can only hold one designated PIS account at a time across all stockbrokers.

- No Intra-day Trading: The RBI strictly prohibits NRIs from engaging in day trading or short selling. All deliveries must be taken.

- Broker Coordination: Your PIS account must be strictly linked with your NRI trading and Demat accounts. Your bank and broker will coordinate to track limits and calculate Capital Gains Tax.

Important Note

Indian regulations have evolved in recent years. Some brokers and banks now offer investment routes where a traditional PIS account may not be required for certain categories of investments. Therefore, before opening accounts, check the latest requirements with your bank, broker, or a qualified financial advisor.

Conclusion

A PIS account has traditionally been a key requirement for NRIs investing in Indian equities through an NRE account. It facilitates regulatory compliance, transaction reporting, and repatriation of funds. By opening an NRE account, PIS account (where required), trading account, and Demat account, NRIs can participate in India’s growing stock market while remaining compliant with applicable regulations.

When people step into the world of trading—whether in stocks, commodities, or derivatives—the most commonly recognized cost is brokerage. Brokerage is the fee charged by a broker for executing buy and sell orders on behalf of the client. While many traders are aware of this expense, it is only one piece of the overall cost structure. In reality, every trade involves multiple charges that can significantly impact net returns if not properly understood.

This blog aims to shed light on the various charges involved in trading so that clients can make more informed financial decisions.

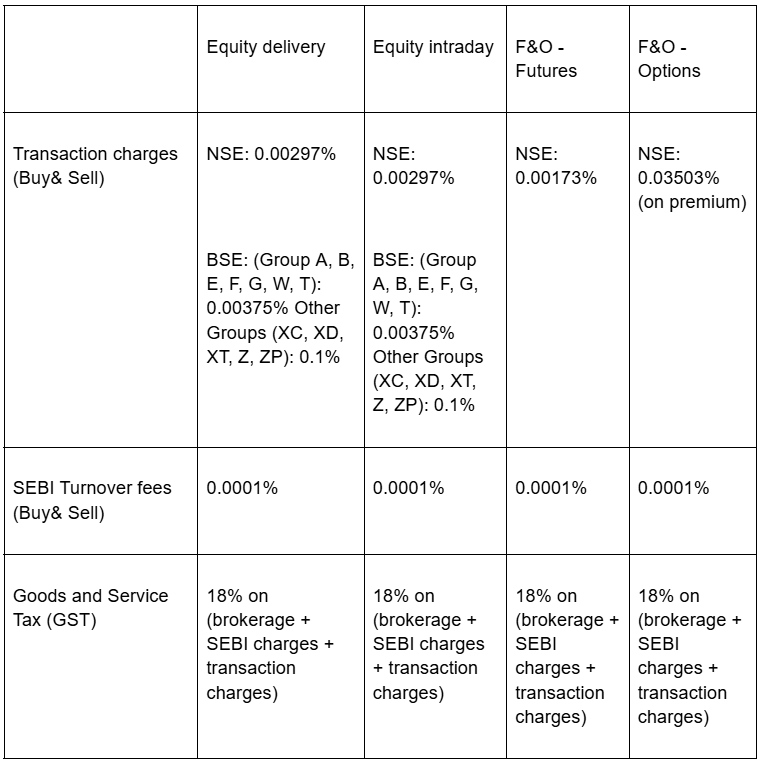

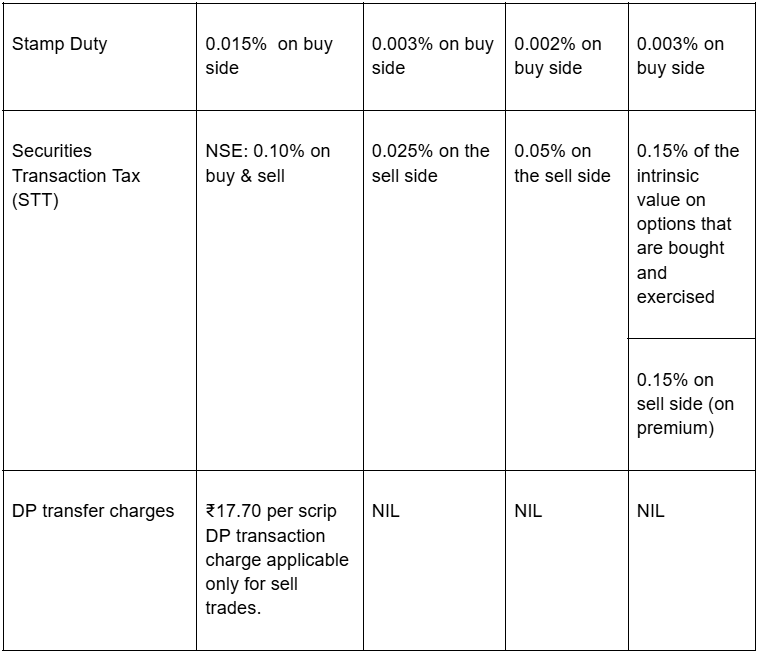

*charges with effect from 01/04/2026

1. Brokerage Charges

Brokerage is the fee levied by brokers for facilitating trades. It can either be a flat fee per transaction or a percentage of the trade value. With the rise of discount brokers, brokerage costs have reduced considerably, but they still remain a key expense.

2. Securities Transaction Tax (STT)

STT is a government-imposed tax applicable on the purchase and sale of securities listed on stock exchanges. The rate varies depending on the type of trade (equity delivery, intraday, or derivatives) and is mandatory for all traders.

3. Exchange Transaction Charges

These charges are levied by stock exchanges for providing the trading platform and infrastructure. Though relatively small, they apply to every trade and add up over time, especially for frequent traders.

4. GST (Goods and Services Tax)

GST is applied to brokerage and exchange transaction charges. Currently, it is charged at a standard rate, increasing the overall cost of trading.

5. SEBI Charges

The Securities and Exchange Board imposes nominal fees on trades to regulate market activities. These charges are minimal but still form part of the total expense.

6. Stamp Duty

Stamp duty is a state government tax applied to the purchase side of a transaction. The rates differ slightly from state to state but are standardized for most financial instruments.

7. DP (Depository Participant) Charges

DP charges are applicable when you sell shares from your demat account. This fee is charged by the depository participant (such as banks or brokers) for handling the transaction.

Why These Charges Matter

While each of these charges may seem small individually, collectively they can reduce overall profitability—especially for active traders who execute multiple trades daily. Ignoring these costs may lead to an overestimation of returns.

Final Thoughts

Understanding all the charges involved in trading is essential for effective financial planning. Brokerage might be the most visible cost, but it is far from the only one. By being aware of additional charges like taxes, transaction fees, and regulatory costs, traders can better calculate their real profits and optimize their trading strategies.

In trading, knowledge is not just power—it’s profit.

Ever Wondered Why Your Trading Account Balance Suddenly Drops to Zero?

You wake up on a Saturday morning, grab your coffee, and log into your stock trading app to review your portfolio. Suddenly, cold sweat hits: your available trading cash reads ₹0.00.

Before you panic and call customer support thinking you’ve been hacked, take a deep breath. Check your primary bank account. You will likely see that exact “missing” amount safely deposited there.

What you just experienced is a regulatory safety feature called the Quarterly Settlement of Accounts (also known as Running Account Settlement).

Here is a straightforward look at what this process is, why it happens, and what you need to know to keep trading smoothly.

What is Quarterly Settlement?

When you trade stocks or derivatives, you transfer money into your broker’s ledger. Often, you might leave uninvested, idle cash sitting in that account waiting for the next market opportunity.

To protect you, the market regulator—SEBI (Securities and Exchange Board of India)—mandates that stockbrokers cannot hold onto your idle cash indefinitely. As per SEBI regulations (Circular Ref: SEBI/HO/MIRSD/DOP/P/CIR/2022/101), stockbrokers are required to transfer any unused funds back to the client’s bank account at regular intervals. This is a standard compliance procedure designed to ensure the safety and transparency of client funds. This standardized the settlement cycle across all stockbrokers to ensure unused funds are returned to your bank account. Once every quarter (or every 30 days if you are an inactive trader), your broker is legally required to pack up all your unused funds and send them right back to your primary bank account.

The Golden Rule: The money is yours. If it’s not actively backing a trade, it belongs in your bank, not your broker’s ledger.

Why Do Regulators Force This Shift?

The policy exists entirely for investor protection.

In the past, some brokerages occasionally misused massive pools of idle client cash to fund their own proprietary operations or prop up other clearing needs. By forcing a clean slate every three months, regulators ensure:

- Absolute Transparency: Capital stays firmly under your control.

- Reduced Broker Risk: Brokerages cannot accumulate unauthorized leverage using client money.

- Account Hygiene: It forces investors to actively look at where their cash is sitting.

What Happens if You Have Active Trades?

A common question is: “If they send all my money back, will my open options or stock positions get squared off?”

No. Your shares and active positions are completely safe.

Retention of Funds

If you have open positions on settlement day, brokers are allowed to retain a specific buffer to ensure your account doesn’t go into a negative balance. Legally, a broker can hold back:

- 100% of your active margin requirement.

- An additional 125% margin buffer to cover potential market swings over the weekend.

- Outstanding Obligations: The exact value of end-of-day obligations across all segments on the day of settlement.

- Client Authorization: The client must specifically authorize the broker to retain funds. Without this, all excess funds must be immediately transferred to the client’s bank account.

A Quick Example Retention due to margin requirements.

Imagine you have ₹5,00,000 sitting in your trading account, but you have an open futures trade requiring ₹2,00,000 in margin.

|

Account Snapshot |

Amount |

|

Total Available Funds |

₹5,00,000 |

|

Active Margin Needed |

₹2,00,000 |

|

Max Allowed Retention (225%) |

₹4,50,000 |

|

Amount Sent to Your Bank |

₹50,000 |

When Does This Take Place?

Settlements are strictly coordinated across the entire financial system. According to the exchanges’ official calendar, settlements happen on the first Friday (or subsequent Saturday) of the new quarter.

The quarterly setoff will be reflected in your ledger as follows:

How to Handle the “Day After”

Because your cash is moved to your bank, your available trading balance will look empty until you transfer it back. If you have automated strategies running or plan to buy stocks early Monday morning, you have to Log in over the weekend or early Monday morning and do a standard UPI or Net banking fund transfer to replenish your trading balance.

The quarterly settlement might feel like a minor logistical chore, but it is one of the strongest regulatory shields keeping your hard-earned capital secure.

A Faster Way to Access Your Investment Statements

We are pleased to introduce a new feature that allows you to download your Capital Gain Report and Portfolio Report directly through the PEN App using your mobile phone or laptop.

This self-service facility enables you to access your investment reports anytime, helping you save time and making your year-end tax filing process more convenient.

-

How to Download Capital Gain or Portfolio Reports

- Step 1:

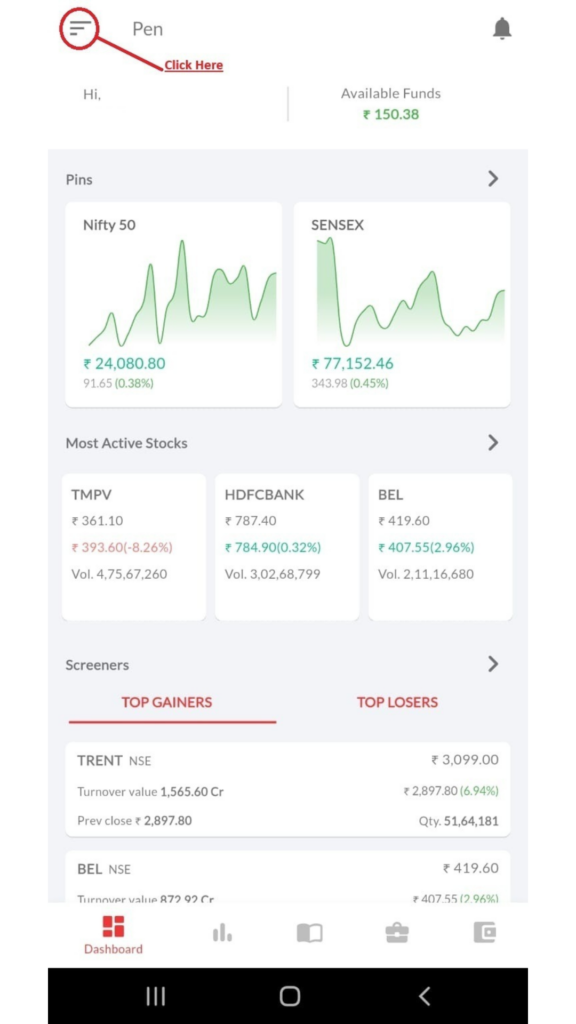

Log in to the PEN App using your Client Code and Password. You may also access the PEN App through your laptop by visiting our website (pentad.in) and logging in.

- Step 2:

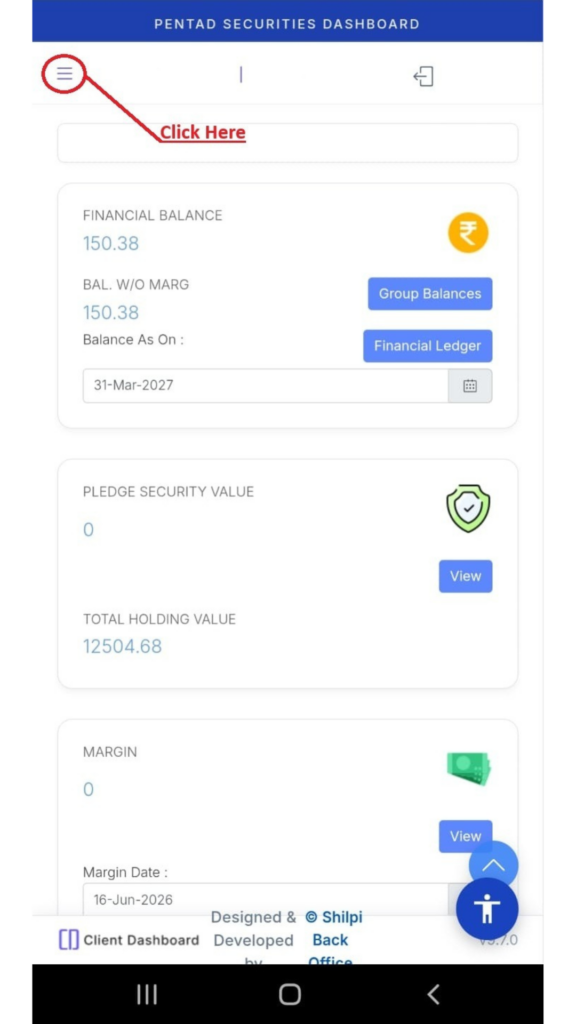

After successful login, the home screen will appear as shown in Image 1.

- Step 3:

Click on the three-line menu (☰) located on the top-left side of the screen as highlighted in Image 1.

Image 1 – PEN App Home Screen

-

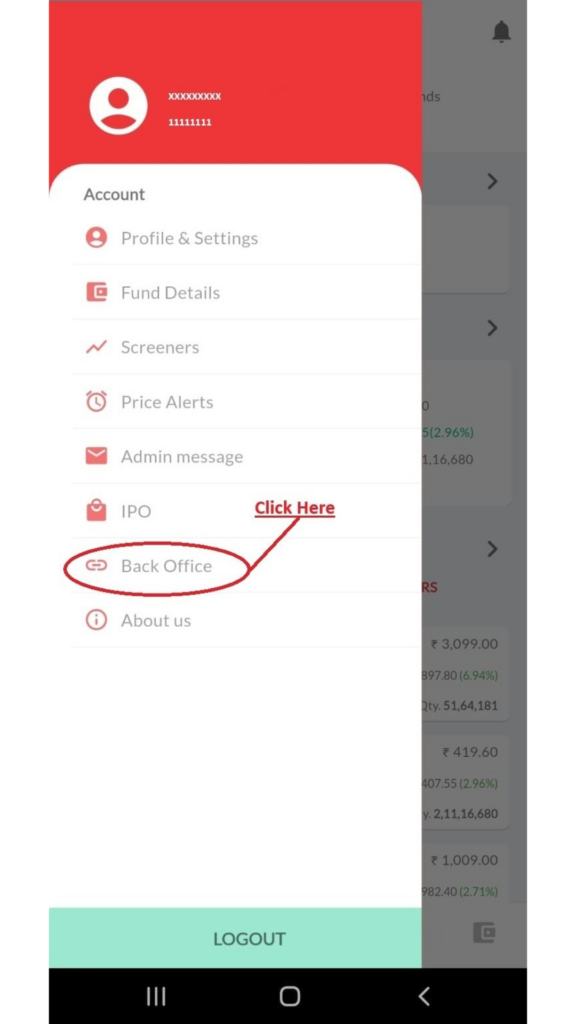

Step 4

- From the menu, click on the Back Office option as shown in Image 2.

Image 2 – Back Office Option

-

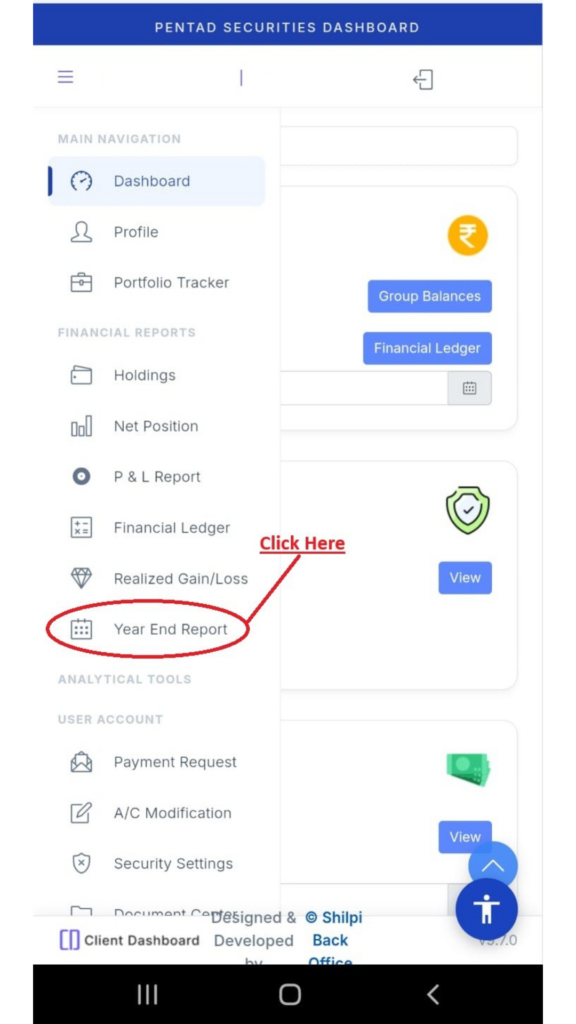

Step 5

- A new page will open. Please wait until the page loads completely. Once the loading is finished, click on the menu icon located at the top-left corner of the screen as shown in Image 3.

Image 3 – Menu Icon .

-

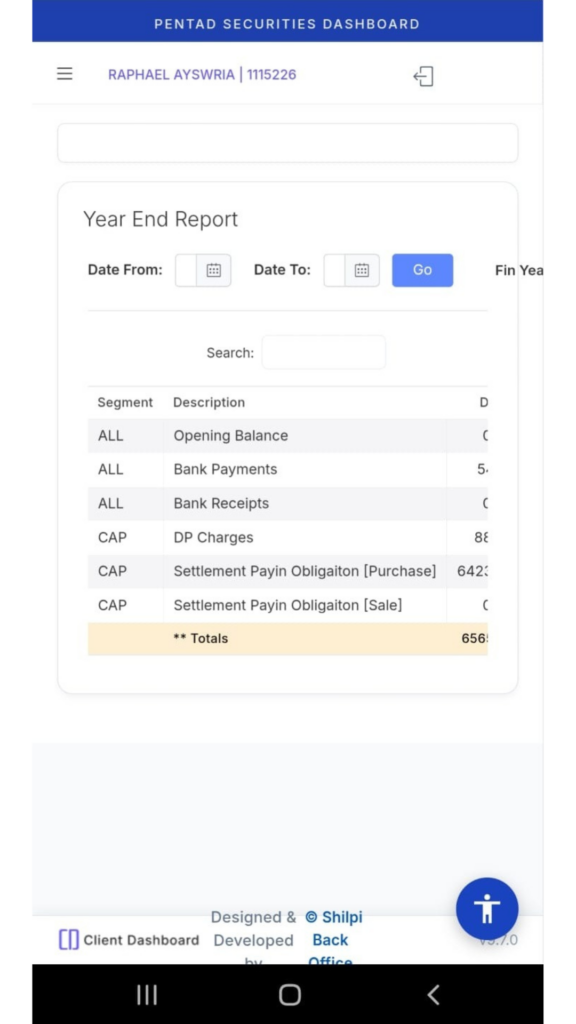

Step 6

- From the left-side navigation panel, click on Year End Report as shown in Image 4.

Image 4 – Year End Report Menu

-

Step 7

- The Year End Summary Report page will be displayed as shown in Image 5.If you are using a mobile phone, please rotate your device to landscape mode for a better viewing experience. If Auto Rotate is disabled, kindly enable it from your phone settings.

Image 5 – Year End Summary Report

-

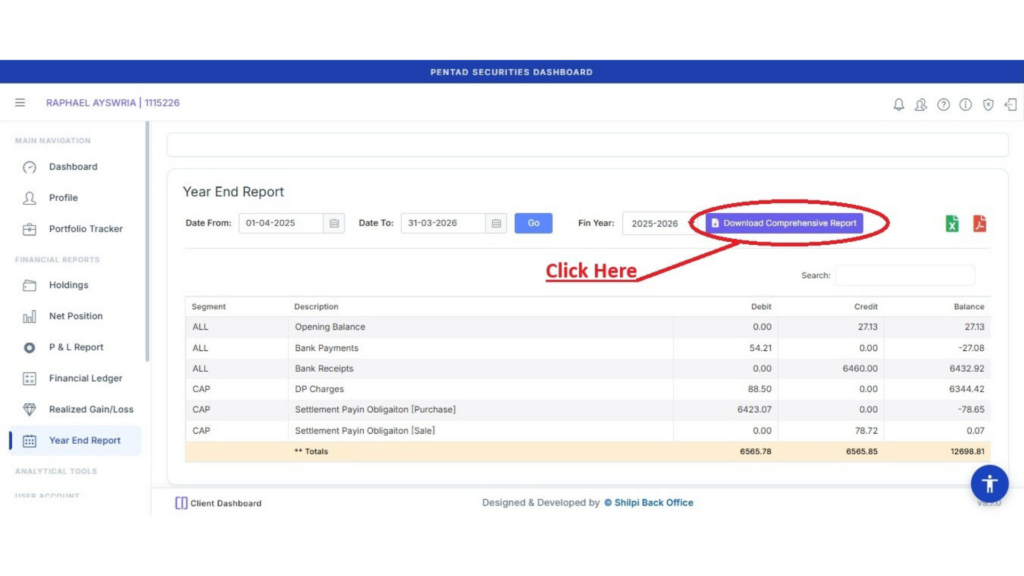

Step 8

- After rotating your phone to landscape mode, click on Download Comprehensive Report as highlighted in Image 6.The report will be automatically downloaded to your device’s Downloads folder in Excel format.

Image 6 – Download Comprehensive Report

Need Assistance?

If you face any issues while downloading the report, please feel free to contact us at operations@pentad.in . Our team will be happy to assist you.

If you’ve ever watched the Indian stock market take a sudden dive, there’s a high chance a spike in global crude oil prices was behind the steering wheel.

For India, oil isn’t just fuel for cars; it’s the lifeblood of the economy. Because India imports roughly 80% to 85% of its crude oil needs, any volatility in global oil markets sends shockwaves straight to Dalal Street.

But why exactly does a surge in oil prices cause such a frenzy in the stock market? Let’s break down the mechanics of this relationship, who wins, who loses, and how you can safeguard your portfolio.

The Macro Picture: Why Oil Matters So Much

When global crude prices climb, it triggers a chain reaction across India’s macroeconomic indicators. Here is how that domino effect hits the stock market:

- The Widening Fiscal Deficit: Buying expensive oil means India has to shell out more US dollars. This widens the Current Account Deficit (CAD), putting immense pressure on the nation’s financial health.

- A Weakening Rupee: As India scrambles to buy dollars to pay for oil, the value of the Indian Rupee ($INR$) depreciates against the $USD$. A weaker rupee makes foreign investors (FIIs) nervous, often leading them to pull money out of Indian equities.

- The Ghost of Inflation: Higher oil prices mean costlier transportation. From the tomatoes in your local market to the raw materials delivered to factories, everything becomes more expensive.

- Interest Rate Hikes: To combat this rising inflation, the Reserve Bank of India (RBI) is often forced to raise interest rates. Higher interest rates make borrowing expensive for companies, squeezing their growth and making stocks look less attractive than fixed-income bonds.

Sector Impact: The Losers and the Winners

A crude oil hike doesn’t affect every stock the same way. While it spells disaster for some sectors, it actually opens up massive opportunities for others.

🔴 The Hardest Hit Sectors (The Losers)

|

Sector |

Why They Suffer |

|

Aviation |

Aviation Turbine Fuel (ATF) accounts for nearly 30–40% of an airline’s operating costs. High oil prices instantly crush profit margins for companies like InterGlobe Aviation (IndiGo). |

|

Paints |

Crude oil derivatives (like monomers and titanium dioxide) make up about 50% of the raw material costs for paint companies. A price hike severely compresses their margins. |

|

Automobiles |

Rising fuel prices increase the “cost of ownership” for consumers, which can dampen the demand for new cars and two-wheelers. |

|

FMCG |

Fast-Moving Consumer Goods companies face a double whammy: raw material costs (like plastic packaging derived from oil) go up, and rural demand drops due to overall inflation. |

🟢 The Silver Lining Sectors (The Winners)

The General Rule: Companies that explore, produce, or refine oil benefit directly from higher prices, as their realization per barrel increases.

- Oil Exploration & Production (E&P): Giants like ONGC and Oil India see immediate benefits because they sell the raw crude they extract at higher global rates.

- Oil Refiners: Companies like Reliance Industries (RIL) and Chennai Petroleum often enjoy higher Gross Refining Margins (GRMs) during oil booms, though this can sometimes be capped by government-imposed windfall taxes.

- Upstream Service Providers: Companies providing drilling rigs, pipes, and offshore services (like Aban Offshore or Jindal Drilling) see increased demand as oil exploration activity picks up globally.

How Should You Navigating an Oil-Driven Market?

As a retail investor, a spike in crude oil shouldn’t panic you into selling everything. Instead, use it as a prompt to re-evaluate your portfolio strategy.

1. Don’t Panic Sell Quality

Market reactions to oil spikes are often knee-jerk. If you hold fundamentally strong companies in the paint or auto sectors with pricing power (the ability to pass costs on to consumers), they will likely recover once oil cycles cool down.

2. Keep an Eye on the Rupee and FIIs

If you see crude rising alongside a massive sell-off by Foreign Institutional Investors (FIIs), it might be wise to hold back on aggressive lumpsum investments and stick to your Systematic Investment Plans (SIPs).

3. Consider Defensive Sectors

When inflation bites and discretionary spending slows down, defensive sectors like Information Technology (IT) and Pharmaceuticals tend to hold up better because their revenues are largely decoupled from domestic oil prices and are earned in US dollars.

The Bottom Line

Crude oil and the Indian stock market share an inverse relationship most of the time: when oil goes up, the Nifty and Sensex usually feel the gravity. However, India’s domestic economy has grown incredibly resilient over the years, backed by strong corporate earnings and robust domestic investor participation. While oil spikes create short-term market turbulence, they also present fantastic buying opportunities for long-term investors who know which sectors will weather the storm.

Disclaimer: This article is for informational purposes only and should not be considered financial advice. Always consult a certified financial advisor before making any investment decisions.

NISM exams are mandatory, SEBI-backed certification tests designed to establish knowledge benchmarks for finance professionals in India. They are essential for securing roles like mutual fund distributor, research analyst, or investment adviser, offering unmatched credibility and regulatory compliance for anyone building a career in the Indian securities markets.

Navigating NISM Exams: Your Gateway to a Thriving Finance Career

If you are looking to build a career in the Indian financial sector, standing out in the crowd requires more than just a degree. Today, financial institutions and regulatory bodies prioritize professionals who not only possess theoretical knowledge but also understand market dynamics and regulatory compliance. Enter the National Institute of Securities Markets (NISM) exams.

Established by SEBI (Securities and Exchange Board of India), NISM aims to raise the bar for market intermediaries. But what exactly are these exams, and why do they hold so much value in the industry? Let’s break it down.

What are NISM Exams?

NISM is a public trust and the educational arm of SEBI. It conducts a series of specialized certification examinations that set the minimum knowledge benchmarks for various professionals working in the Indian securities markets.

There are over 20 different modules tailored to specific financial domains, including:

- Mutual Funds: (e.g., NISM Series V-A) Mandatory for distributing mutual funds.

- Research & Advisory: (e.g., NISM Series XV and X-A/B) Mandatory for Research Analysts and Investment Advisers.

- Derivatives & Operations: (e.g., Equity Derivatives, Currency Derivatives) Essential for dealers and risk managers.

The Real Value of NISM Certifications

Whether you are a fresh graduate or an experienced professional looking to switch careers, passing NISM exams carries significant weight:

1. They are Mandatory by Law

In India, you cannot legally perform certain financial jobs without the corresponding NISM badge. For instance, if you want to become a SEBI-Registered Investment Advisor (RIA) or a Research Analyst, passing the NISM Series X-A/B and Series XV exams is legally required.

2. Immediate Career Differentiator

Leading banks, brokerages, and wealth management firms in Kochi and across India prefer—and often require—NISM-trained talent for client-facing roles. Holding multiple certifications signals to employers that you are a “Zero Risk” hire.

3. Stackable Skill Paths

The NISM ecosystem allows for “stackable” learning. You can start with basic entry-level exams (like the Foundation or Mutual Fund Distributors module) and work your way up to advanced expert modules (like Alternative Investment Funds). This cumulative progression creates a tailored, highly attractive CV.

4. Credibility and Trust

When your certification originates from SEBI itself, it immediately builds trust with your clients. It proves that you have an objective, regulated understanding of financial products, risk, and fiduciary duties.

How to Approach NISM Exams

Preparing for NISM exams is highly structured, affordable, and accessible. Here is how you can get started:

1. Visit the Official Source: Registration and exam scheduling are done directly through the NISM Online Portal. You can also view available slots and locations across the country.

2. Utilize Official Study Materials: NISM provides excellent workbooks for each module, which are downloadable or available for online reading at no cost.

3. Practice with Mock Tests: To conquer exam anxiety, simulate real testing conditions by utilizing mock test platforms prior to your exam day.

Conclusion

A NISM certification is much more than just a passing certificate; it is the fundamental building block of a compliant and lucrative career in finance. Whether you aim to advise clients, analyze equities, or manage portfolios, these badges open doors in a rapidly expanding financial market.

Meaning, Types, Detailed Process & Key Benefits

In India’s modern securities market, shares are held and transferred electronically through depositories instead of physical certificates. This system ensures faster settlement, higher security, and complete regulatory transparency.

Share transfer through depositories is carried out via:

- Central Depository Services Limited (CDSL)

- National Securities Depository Limited (NSDL)

Both operate under the supervision of the Securities and Exchange Board of India (SEBI).

In simple terms:

👉 It is the digital transfer of shares between Demat accounts.

Why Is Share Transfer Through Depositories Important?

The depository system was introduced to eliminate problems associated with physical share transfers.

Key Reasons:

1️⃣ Eliminates Physical Risks

No loss, theft, forgery, or damage of share certificates.

2️⃣ Faster Settlement

Transfers are completed within 1 working day in most cases.

3️⃣ Regulatory Protection

Transactions are monitored under SEBI regulations.

4️⃣ Transparency

Investors receive instant SMS/email alerts for debit and credit.

5️⃣ Reduced Fraud

Unique ISIN-based identification prevents manipulation.

Types of Share Transfer Through Depositories

1️⃣ On-Market Transfer

This occurs when shares are bought or sold through a stock exchange.

How It Works:

- Investor places buy/sell order.

- Trade is executed.

- On settlement day (T+1/T+2), shares are automatically debited from seller and credited to buyer via depository.

✔ Fully automated

✔ No manual instruction required

2️⃣ Off-Market Transfer

Direct transfer between two Demat accounts without using the stock exchange.

Common Reasons:

- Gift to family member

- Transfer between own accounts

- Private transaction

- Corporate restructuring

Requires submission of Delivery Instruction Slip (DIS) or online instruction.

3️⃣ Inter-Depository Transfer

Transfer between accounts held in different depositories.

Example:

- Sender in CDSL

- Receiver in NSDL

Requires accurate DP ID and ISIN details.

4️⃣ Intra-Depository Transfer

Transfer within the same depository (CDSL to CDSL or NSDL to NSDL).

Usually processed faster than inter-depository transfers.

Detailed Process of Share Transfer Through Depositories

Below is the structured step-by-step process (mainly for off-market transfer):

Step 1: Initiating the Transfer Request

The transferor submits a request to their Depository Participant (DP), mentioning:

- Purpose of transfer

- Transferee’s Demat account details

- Type of transfer (gift, family, correction, etc.)

Step 2: Submission of Required Details

Mandatory information includes:

- ISIN (International Securities Identification Number)

- Quantity of shares

- Target DP ID & Client ID

- Execution date

- Reason for transfer

Step 3: Verification by DP / Depository

The DP verifies:

- Signature match

- Demat account status

- Available balance

- KYC compliance

- Freeze or lien marking.

Step 4: Processing Through CDSL / NSDL System

After verification:

- Instruction is entered into the depository system.

- For inter-depository transfers, coordination between both depositories takes place.

Step 5: Debit and Credit of Shares

Once approved:

- Shares are debited from transferor’s Demat account.

- Shares are credited to transferee’s Demat account.

- SMS/email confirmation is sent to both parties.

Time Taken for Share Transfer

Normal processing time for both CDSL and NSDL

- Intra-depository transfer:usually within few hours to 1 working day.

- Inter-depository transfer:usually 1-2 working days

Delays may occur if details are incorrect, or documents are incomplete.

Key Benefits of Share Transfer Through Depositories

✅ High Security

Electronic holding eliminates forgery and fake certificates.

✅ Faster Processing

Quick settlement compared to physical transfer (which earlier took months).

✅ Complete Transparency

Real-time alerts and transaction tracking.

✅ Easy Record Maintenance

All transactions are digitally recorded and auditable.

✅ Simplified Nomination & Transmission

Smooth transfer in case of death of account holder.

✅ Reduced Paperwork

Minimal documentation compared to old physical system.

Common Reasons for Rejection

- Incorrect ISIN

- Wrong DP ID / Client ID

- Signature mismatch

- Insufficient balance

- Account freeze

Proper verification before submission helps avoid rejection.

Frequently Asked Questions (FAQs)

1. What is an off-market share transfer?

An off-market transfer is the transfer of shares between two demat accounts without executing a trade on the stock exchange.

2. Can shares be transferred between CDSL and NSDL?

Yes. Shares can be transferred between CDSL and NSDL through an inter-depository transfer facilitated by a broking firm.

3. Is selling shares required to transfer them?

No. Shares can be transferred without selling by using the off-market transfer process.

4. How long does it take to transfer shares?

Usually, 1 working day for same depository transfers/interdepository transfers

5. Are there charges for transferring shares?

Yes. DP charges, inter-depository fees, and applicable stamp duty may apply.

6. Can shares be gifted to family members?

Yes. Shares can be gifted to relatives or family members through a broking firm with proper documentation.

7. What happens to shares after the death of a holder?

Shares are transferred to the nominee or legal heirs through the transmission of shares process.

8. Is PAN mandatory for share transfer?

Yes. PAN and KYC compliance are mandatory for both transferor and transferee.

9. Can I transfer shares online?

Many broking firms allow online off-market transfer requests, subject to account activation and approvals.

10. Why should I use a broking firm for share transfer?

A broking firm ensures regulatory compliance, reduces errors, and provides expert support throughout the process.

Conclusion

Share transfer through depositories has revolutionized the Indian capital market by introducing a secure, transparent, and efficient system for transferring securities. Whether on-market or off-market, the electronic framework ensures regulatory compliance, reduced risk, and faster settlement.

Understanding the types, process, and operational requirements helps investors and financial professionals ensure smooth and error-free transactions within the depository ecosystem.

If you trade in the Indian stock market—especially in segments like intraday or derivatives—you’ve likely come across the term margin. Margins are a crucial part of the trading ecosystem, acting as a safety buffer for brokers and exchanges against potential losses.

However, many traders find margin concepts confusing due to the different types involved. This blog simplifies the various types of margins collected by stockbrokers in India and explains how they impact your trading.

Margin in Trading

Margin is the amount of money a trader must deposit with a broker to take a position in the market. It ensures that traders can meet their obligations in case the market moves against them.

Margins are regulated by exchanges like the National Stock Exchange (NSE) and Bombay Stock Exchange (BSE), along with the Securities and Exchange Board of India (SEBI).

Why Do Brokers Collect Margins?

Margins serve multiple purposes:

* Protect brokers from client defaults

* Reduce systemic risk in the market

* Ensure discipline among traders

* Provide leverage opportunities

Types of Margins in India

1. SPAN Margin

*SPAN (Standard Portfolio Analysis of Risk) is a system used by financial exchanges to calculate the initial margin required for Futures and Options (F&O) trading. It evaluates an entire trader’s portfolio to estimate the maximum probable loss over a single trading day, adjusting dynamically based on market volatility

It is calculated using a risk-based model that considers:

* Price volatility

* Time to expiry

* Market conditions

Where It Applies

* Futures

* Options (especially for sellers)

SPAN margin ensures that your position is protected against worst-case scenarios.

2. Exposure Margin

An Exposure Margin is an additional safety buffer charged by stock exchanges over and above the standard SPAN margin in derivatives trading. It acts as an extra layer of protection to safeguard brokers and the exchange against sudden, extreme market movements or credit risks that the primary margin model might miss.

Acts as a cushion against unexpected market volatility.

* Fixed percentage of contract value

* Mandatory for derivatives trading

Example

If SPAN margin is ₹1,00,000, exposure margin might be ₹30,000 extra.

3. Initial Margin

Initial margin is the upfront collateral or cash an investor must deposit with a broker to open a leveraged position. It acts as a “good faith” security deposit, allowing the trader to control a much larger asset value than their actual account balance while protecting the broker against potential losses.

The total margin required to initiate a trade.

*Initial Margin = SPAN Margin + Exposure Margin*

You must have this amount available before placing a trade.

4. Maintenance Margin

Maintenance margin is the minimum equity an investor must keep in a margin account to hold borrowed positions. If the account value falls below this threshold due to losses, brokers issue a margin call requiring the investor to add more funds or close positions to prevent forced liquidation

What Happens If You Fall Below?

* Broker issues a margin call

* You must add funds or square off positions

5. Mark-to-Market (MTM) Margin

Mark-to-Market (MTM) margin is the daily settlement of unrealized profits and losses on open futures and derivative positions based on the exchange’s closing prices. At the end of every trading day, your account balance is adjusted to reflect the current market value. If the MTM process results in a loss that dips below your required maintenance margin, the broker will require you to deposit additional funds.

* Profits are credited daily

* Losses must be paid immediately

Prevents accumulation of large losses over time.

6. Peak Margin

Peak margin is the highest margin requirement recorded across multiple random snapshots of a trader’s open positions taken throughout a single trading day. Introduced by SEBI to prevent excessive leverage, it mandates that traders maintain adequate upfront funds at all times to cover their maximum intraday exposure

* Margin is checked multiple times during the day

* Traders must maintain margin at all times

Impact

* Reduced excessive leverage

* Increased transparency

7. Value at Risk (VaR) Margin

Value at Risk (VaR) margin is an upfront risk-based deposit required by exchanges to cover the maximum expected loss on a trading portfolio over a specific time horizon. It is calculated using statistical volatility models to ensure that an investor’s account has enough funds to survive normal, adverse market movements on 99% of trading days.

Where It Applies

* Primarily in equity delivery and intraday trading

Why It Matters

Ensures coverage for typical market fluctuations.

8. Extreme Loss Margin (ELM)

Extreme Loss Margin (ELM) is an additional risk buffer charged by financial exchanges to cover potential financial losses from rare, highly volatile market movements. It acts as a safety net over standard risk models like Value at Risk (VaR)

9. Delivery Margin

Delivery margin refers to the upfront cash or collateral that an investor must maintain in their trading account when buying or selling stocks for long-term delivery. While buying equity requires 100% upfront funds, selling holdings temporarily blocks a portion of the credit (usually 20%) to safeguard against settlement defaults. This ensures market stability and prevents excessive leverage across portfolios

* Usually lower risk compared to intraday

* Still requires upfront funds

10. Intraday Margin

Intraday margin is a temporary credit facility provided by brokers that lets you buy or sell securities using a small fraction of your own capital. It gives you greater purchasing power to amplify potential profits during the day ).

Benefit

* Higher leverage

* Lower capital requirement

Risk

* Higher exposure to volatility

Key Changes in Margin Rules in India

In recent years, the Securities and Exchange Board of India introduced stricter margin rules:

* Mandatory upfront margin collection

* Peak margin reporting

* Reduced leverage for traders

These changes aim to make markets safer and more stable.

* Always maintain extra margin to avoid forced liquidation

* Monitor margin requirements regularly

* Avoid over-leveraging

* Understand risks before trading derivatives

* Use broker platforms to track real-time margin

Margins are the backbone of risk management in the stock market. While they enable traders to take larger positions, they also come with responsibilities and risks.

Understanding the different types of margins—like SPAN, Exposure, MTM, and Peak Margin—can help you trade more safely and efficiently in the Indian markets.

In trading, it’s not just about profits—it’s about managing risk smartly. And margins are your first line of defence.

If you’ve recently moved back to India after living abroad, you’ve likely faced the challenge of converting your financial accounts. Today, we’re tackling a crucial one: How to convert your NRI trading and Demat account to a Resident account!

Under FEMA regulations, your NRI accounts cannot remain as they are once you become a Resident Indian, so let’s walk through the mandatory steps you need to take with your broker, or Depository Participant (DP), and your bank.

Step 1: Notify Your Authorities

The very first thing you need to do is inform the right people immediately after you become a Resident Indian.

- Notify your DP (Broker): You must inform your Depository Participant about your change in residential status—from NRE/NRO to Resident Indian.

- Inform your PIS Bank: Also, make sure to inform your bank and close your Portfolio Investment Scheme (PIS) account.

Step 2: The Paperwork and Documentation

Next up is gathering all your documents. You’ll need to submit an application along with several supporting proofs to your DP.

|

Document Category |

Required Documents (Common Examples) |

|---|---|

|

Application Forms |

Account modification form – Annexure 3.1 (provided by your DP) |

|

Account closure form for the existing NRE/NRO Trading account. |

|

|

New Resident trading application form. |

|

|

Identity Proof |

Self-attested copy of your PAN card. |

|

Address Proof |

Self-attested copy of your Indian address proof (e.g., Driving license, Passport, Voter ID, Masked Aadhaar). |

|

Bank Proof |

Proof for linking the new resident savings account (e.g., self-attested personalized cancelled cheque or bank statement showing account number, MICR, and IFSC). |

|

Income Proof |

Required if you wish to trade in derivatives (F&O). This can be a 6-month bank statement with an average balance above ₹10,000, or a salary slip, ITR acknowledgement, or net worth certificate. |

Step 3 & 4: Compliance and Status Change

Once your paperwork is submitted, your broker takes over two key steps:

- Re-KYC: Your DP will require a fresh Know Your Customer (KYC) update reflecting your new resident status.

- Change of Account Status: The DP will then modify your official account status to “Resident individual”.

Step 5: Account Closure and Opening

This is the most critical step to understand: Your existing NRE/NRO trading account cannot be converted into a Resident account.

- Instead, your broker will close the NRE account after collecting all the required applications.

- They will simultaneously open a brand-new Resident trading account for you.

Key Takeaways You Must Remember!

Finally, here are two extremely important points regarding your investments during this transfer:

1. No Taxable Event: The transfer of securities from your old NRI Demat to your new Resident Demat is not a taxable event. You do not owe capital gains tax just for making the transfer.

2. Cost of Acquisition: Your original cost of acquisition for tax purposes remains the same. It does not reset, meaning your capital gains calculation will use the price you initially paid for the shares.

Dividend investing is a strategy where investors buy shares of companies that regularly share a portion of their profits with shareholders. This payment is called a dividend.

Instead of earning only when the stock price rises, dividend investors can also receive regular income while holding the stock.

How Dividend Investing Works

When you buy shares of a dividend-paying company:

- You become a shareholder

- The company may pay dividends quarterly, half-yearly, or annually

- You receive money directly to your bank account or brokerage account

Example:

If a company announces ₹10 dividend per share and you own 100 shares:

100 × ₹10 = ₹1,000 dividend income

Why Investors Like Dividend Investing

1. Regular Passive Income

Useful for retirees or people wanting extra income.

2. Long-Term Wealth Creation

Reinvesting dividends can significantly grow wealth over time.

3. Stable Companies

Many dividend-paying companies are mature and financially strong.

4. Less Stress

You earn income even if stock prices move slowly.

Best Types of Dividend Stocks

Look for companies with:

- Consistent profits

- Regular dividend history

- Strong cash flow

- Low debt

- Good management

Common sectors:

- Banking

- FMCG

- IT

- Utilities

- Energy

Important Terms to Know

Dividend Yield

Annual dividend compared to share price.

If stock price = ₹200

Annual dividend = ₹10

Dividend Yield = 5%

Payout Ratio

How much profit is paid as dividends.

Lower to moderate payout ratios can be healthier.

Dividend Investing Example

Imagine investing ₹1,00,000 in quality dividend stocks with 4% average yield.

You may receive around:

₹4,000 yearly income

(plus, possible stock price growth)

Risks of Dividend Investing

- Dividends are not guaranteed.

- Company profits can fall.

- Stock price can drop.

- High yield stocks can be risky traps.

Best Strategy for Beginners

- Choose quality companies.

- Diversify across sectors.

- Reinvest dividends.

- Stay invested long term.

- Avoid chasing very high yields.

Is Dividend Investing Good in India?

Yes, especially for long-term investors who want both income and growth. Many Indian companies have solid dividend histories.

Final Thoughts

Dividend investing is a smart way to build wealth slowly while receiving regular income. It suits patient investors more than quick traders.