Investing is an important step towards financial success, and mutual funds are among the most popular investment options. However, many investors are typically perplexed by Mutual Funds and Systematic Investment Plans (SIPs). While they are interconnected, they perform distinct roles in wealth development.

A mutual fund is an investment vehicle, whereas a SIP is a way to invest in mutual funds. Understanding the fundamental differences between them will help you make more informed financial decisions. In this blog, we will compare SIPs and Mutual Funds, highlighting their differences and benefits and determining which one best suits your investment strategy.

You may also like to read:

- Mutual Funds: Different Types and Mechanics Behind NAV Calculation

- Risk Management in Derivative Trading: Strategies and Techniques

- Halal Investing: Balancing Financial Growth with Ethical Values

What is SIP?

A Systematic Investment Plan (SIP) is an investment strategy that allows individuals to invest a fixed amount of money at regular intervals, such as monthly or quarterly, into a mutual fund scheme. This disciplined approach facilitates gradual wealth accumulation and instils financial discipline among investors.

How do SIPs work?

When you enrol in an SIP, a predetermined amount is automatically debited from your bank account and invested in a selected mutual fund. This process is continuous for a specified period or until you terminate the plan. Each contribution purchases units for the mutual fund based on the prevailing Net Asset Value (NAV), accumulating units over time.

6 Types of SIPs

1. Regular SIPs: This is the most common type of SIP where the investors contribute a fixed amount at regular intervals (monthly, quarterly, or annually).

2. Step Up SIP: Among different types of SIPs, this allows investors to increase their investment amount periodically (e.g., annually).

3. Flexi SIP: This SIP provides flexibility to investors to increase or decrease the investment amount based on their financial situation or market conditions.

4. Trigger SIP: The trigger SIP allows investors to set predefined conditions for investment, such as NAV-based index-based, or time-based triggers.

5. Perpetual SIP: This SIP does not have a fixed tenure; instead, the investment is continuous indefinitely until the investor manually stops it.

6. Multi SIP: A multi SIP allows investors to invest in multiple mutual fund schemes through a single SIP mandate.

4 Benefits of SIPs

1. Rupee Cost Averaging: This approach facilitates cost averaging, as more units are acquired when prices are down and fewer when prices are up. It also reduces the impact of market volatility on investment.

2. Power of Compounding: Regular investments and reinvestments of returns can lead to significant wealth accumulation over the long term as earnings generate their earnings.

3. Financial Discipline: Automated, regular contributions promote disciplined saving habits, ensuring consistent investments without the need for active decision-making.

4. Flexibility: Investors can choose the investment amount, frequency, and duration of the SIP. Many mutual funds allow SIPs with amounts as low as ₹500 per month, making them accessible to a wide range of investors.

What are Mutual Funds?

Mutual funds offer a way for investors to collectively invest in a diversified portfolio of stocks, bonds, or other securities. This approach allows investors to access professionally managed portfolios, benefiting from diversification and economies of scale.

How do Mutual Funds Work?

When you invest in a mutual fund you purchase units of the fund, each representing a fraction of the fund’s holdings. The value of these units is determined by the Net Asset Value (NAV), which fluctuates based on the market value of the underlying assets. Professional fund managers oversee the portfolio, making investment decisions aligned with the fund’s objectives.

4 Types of Mutual Funds

Mutual Funds can be categorised based on their structure and management style:

1. Open Ended Funds: This allows the investors to buy and redeem units at any time and this provides liquidity and flexibility.

2. Close-End Funds: These funds have a fixed number of units and are traded on stock exchanges. Investors can buy or sell units in the secondary market.

3. Actively Managed Funds: Fund managers actively select securities to outperform the market.

4. Passively Managed Funds: These funds replicate a market index, aiming to match its performance.

4 Benefits of Investing in Mutual Funds

1. Diversification: investing in a variety of assets at the same time reduces the impact of any single investment’s poor performance on the overall portfolio.

2. Professional Management: Experienced fund managers make informed investment decisions on behalf of investors.

3. Affordability: Mutual funds offer a way to diversify investments, making it achievable for investors with modest budgets.

4. Liquidity: Open-ended mutual funds offer the flexibility to redeem units at the current NAV, providing easy access to funds.

You may also like to read:

- Best Investment Options in India for NRIs in 2025

- Direct vs. Regular Mutual Fund: Which One to Choose

- 11 Child Investment Plans in 2025: Investing for Your Child’s Future – Guide

6 Key Differences Between Mutual Funds and SIPs

When it comes to investment, mutual funds and Systematic Investment Plans (SIPs) are often mentioned together. Both of them are connected but they serve different purposes. Understanding their difference can help the investors make the correct decision.

1. Investment Approach

- Mutual Funds: Investors can invest a lump sum or opt for a structured investment strategy.

- SIP: It follows a disciplined investment approach, allowing investors to contribute small amounts regularly.

2. Mode of Investment

- Mutual Funds: Investors have the option to invest in a lump sum or through SIP.

- SIP: It is a systematic mode of investing in mutual funds, helping in cost averaging and disciplined investing.

3. Market Risk Exposure

- Mutual Funds: A lump-sum investment in mutual funds is more susceptible to market volatility as the entire amount is invested at once.

- SIP: It reduces risk by spreading the investment over time, leveraging the benefit of rupee cost averaging.

4. Affordability and Accessibility

- Mutual Funds: It requires a larger initial investment if investing in a lump sum.

- SIP: More accessible for beginners as it allows investment with a lower amount periodically.

5. Flexibility

- Mutual Funds: Investors can enter or exit based on their financial goals, but timing the market is crucial in lump-sum investments.

- SIP: Offers flexibility in investment amount and tenure, allowing investors to adjust contributions as needed.

6. Return and Compounding

- Mutual Funds: A lump-sum investment may yield higher returns if the market performs well during the investment period.

- SIP: Benefits from longer-term compounding, making it suitable for wealth creation over time.

Conclusion

Understanding the nuances between SIPs and mutual funds is crucial for making informed investment decisions. While a mutual fund is an investment product, a SIP is simply a method of investing in it. SIPs offer a disciplined and systematic approach, ideal for long-term goals and mitigating market volatility through rupee-cost averaging. Mutual funds, on the other hand, provide a broader spectrum of investment options catering to various risk appetites and financial objectives.

The decision to invest via a SIP or a lump sum in a mutual fund ultimately depends on individual circumstances, such as financial goals, risk tolerance, and investment horizon. By carefully considering these factors and understanding the characteristics of both SIPs and mutual funds, investors can effectively navigate the investment landscape and work towards achieving their financial aspirations.

Knowing how SIPs and mutual funds differ from one another is only the first step. Pentad Securities offers a range of investment strategies designed to cater to both experienced and new investors. Our goal is to assist you in identifying solutions that strike a balance between growth potential, returns, and safety. Get in touch with us right away to learn more about our investment options and how we can help you reach your financial goals.

India has long been a preferred destination for Non-Resident Indians (NRIs) looking to invest their hard-earned money. With its robust economy, favourable investment policies, and growing financial market, India offers a variety of opportunities to help NRIs diversify their portfolios. If you are an NRI exploring investment options in 2025, here is your ultimate guide.

You may also like to read:

- Risk Management in Derivative Trading: Strategies and Techniques

- Halal Investing: Balancing Financial Growth with Ethical Values

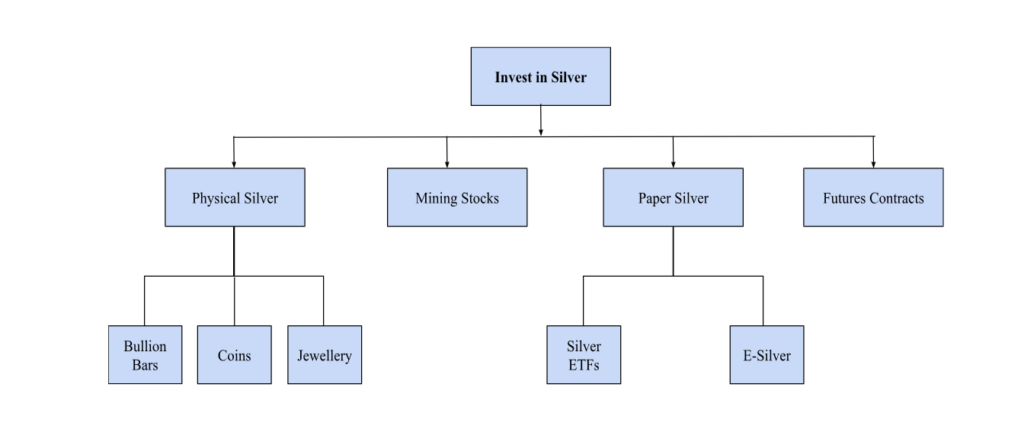

- How to Invest in Silver in India – Smart Ideas from Pentad

Top Investment Options for NRIs in 2025

1. Mutual Funds

Mutual funds remain one of the most versatile investment options for NRIs. They offer opportunities to invest in equity, debt, or hybrid funds, catering to varying risk appetites. NRIs can invest through NRE or NRO accounts and enjoy tax-efficient returns, especially in equity-linked schemes.

The investments for the same need to be done in the Indian currency and not the foreign ones. Return rates offered on the mutual funds in India depend upon the type of fund invested.

2. Fixed Deposits (FDs)

Fixed Deposits are often the go-to choice for NRIs who prefer low-risk investments with guaranteed returns. What makes FDs stand out is their simplicity and reliability. You deposit a sum of money for a fixed tenure, and in return, you earn interest at predetermined rates.

NRIs can choose from special types of FDs like NRE (Non-Resident External) and NRO (Non-Resident Ordinary) accounts for different needs.

- NRE FDs: Ideal for parking foreign earnings in India with tax-free interest and repatriability.

- NRO FDs: Perfect for managing income earned in India, like rent or dividends, with attractive interest rates.

- FCNR FDs: A great option for earning in foreign currency while avoiding exchange rate risks.

3. National Pension Systems (NPS)

The National Pension System (NPS) is a government-regulated retirement savings scheme open to NRIs. It ensures long-term financial security while offering flexibility in investments.

- Tier I Account: A mandatory retirement account with tax benefits under Section 80C.

- Tier II Account: A voluntary savings account with no lock-in period.

- Choice of Funds: Select equity, debt, or a mix based on your risk appetite.

NPS is a smart way for NRIs to ensure a stress-free retirement while enjoying the advantage of disciplined savings.

4. Real Estate

Indian real estate has always been a lucrative investment for NRI’s. From residential properties to commercial spaces, the options are endless.

- High Returns: Property prices in metropolitan areas and Tier-2 cities show consistent appreciation.

- Rental Income: Earn steady rental returns while your property value increases over time.

- Regulated Market: The introduction of RERA has increased transparency and trust in real estate transactions.

Now it is totally upon you if you want to use the investment for personal use or investment, real estate in India is undoubtedly an asset that promises tangible and long-term benefits.

5. Gold Investments

Gold is not just a cultural staple, it is also an excellent financial asset. NRIs can invest in physical gold, gold ETFs, or sovereign gold bonds. If you’re still wondering why gold, we would love to help you figure that out;

It is a hedge against inflation and economic uncertainty and sovereign gold bonds offer interest along with price appreciation. Gold ETFs are a modern way to invest in gold without the hassle of storage.

Gold investments have a never-ending relevance and can anchor your portfolio with stability and liquidity.

You may also like to read:

- A Comprehensive Guide to Gold Hedging: Protecting Your Investments

- How to Invest in Sovereign Gold Bond

- Direct vs. Regular Mutual Fund: Which One to Choose

6. Alternative Investment Funds or AIF’s

AIFs cater to sophisticated investors who are open to exploring innovative avenues. They include private equity, hedge funds, and venture capital investments.

- Higher Returns: Potential for significant gains in niche markets.

- Diversification: Access to unique asset classes beyond traditional stocks and bonds.

- Professional Management: Investments managed by experts with in-depth market knowledge.

AIFs are ideal for NRIs looking to diversify their portfolios and target high-growth opportunities.

7. PPF

The PPF is a long-term savings scheme backed by the Indian government, offering safety and tax benefits. Although NRIs can’t open a new PPF account, existing accounts can be maintained. We are happy to walk you through the various perks of PPF as an NRI investment option in India;

- Attractive Interest Rates: Earn compounded interest on your savings.

- Tax-Free Growth: Maturity proceeds and interest are completely tax-free in India.

- Lock-in Period: A disciplined approach to long-term savings with a 15-year tenure.

For NRIs with an existing PPF account, it’s a great way to ensure tax-efficient growth.

Read more about:

- SIP Investments – A Comprehensive Guide

- Investment Plans for Housewives: Smart Strategies for Financial Independence

- Mutual Funds: Different Types and Mechanics Behind NAV Calculation

8. NSC (National Savings Certificate)

The NSC is a government-backed fixed-income scheme, making it one of the safest investment options.

- Guaranteed Returns: Fixed interest rates ensure predictable growth.

- Tax Benefits: Eligible for deductions under Section 80C of the Income Tax Act.

- Short Lock-In: The 5-year lock-in period is perfect for medium-term goals.

NSCs, to be very precisely said, are simple, secure, and tailored for conservative investors.

9. Unity Linked Insurance Plans

ULIPs combine life insurance with market-linked investments, hence offering the very best of both worlds. Let us check out some of the merits of ULIPs;

- Flexible Investments: Allocate funds between equity and debt as per your risk profile.

- Tax Savings: You get to enjoy tax deductions under Section 80C.

- Long-term Benefits: Create a financial safe space by securing the future of your family.

ULIPs offer financial growth and don’t have to be complex at all, which makes them a well-rounded investment choice for NRIS.

10. Child Investment Plans

Child Investment Plans help you save systematically to secure your child’s education and other milestones. They are one of the best NRI investment plans in India. There are multiple benefits of investing in child plans as NRIs;

- Assured Payouts: Guaranteed financial support at key stages of your child’s life.

- Insurance Cover: In case of your untimely demise, your child will receive a lump sum amount to cover their life expenses. Protect your child’s future even in your absence.

- Flexible Benefits: Payouts can be customised to align with major expenses like higher education.

These plans are a thoughtful way to ensure that your child’s dreams are never compromised.

11. Capital Guarantee Solution Plans

The Capital Guarantee Solutions Plans protect your principal investment while offering steady returns.

- Safety First: Ideal for conservative investors who prioritise capital preservation.

- Reliable Growth: Guaranteed returns ensure that your money grows steadily.

- Flexible Tenures: Choose a plan that aligns with your financial goals.

For risk-averse NRIs, these plans provide assured growth.

12. Guaranteed Returns Traditional Plans

If it is predictability that you’re most concerned about, traditional guaranteed return plans are perfect for you. Check out the merits of Guaranteed Returns Traditional plans as listed below;

- Fixed Benefits: Assured payouts from the plans provide financial security.

- Bonus Additions: Many plans offer loyalty or performance bonuses.

- Long-Term Planning: These plans are ideal for funding future expenses like education or retirement.

These plans are highly dependable for NRIs seeking risk-free, long-term savings.

13. Equity Investment

India’s equity markets are a renowned hotspot for growth, which makes them immensely attractive for NRI investors. The undeniable merits of equity market investments are as mentioned below;

- High Returns: Invest in the booming sectors such as healthcare, technology and infrastructure.

- Flexibility: Choose between direct stocks or mutual funds.

- Global Access: Seamless participation through NRE or NRO accounts.

Equity investments are ideal for NRIs who can bear the risk it takes for the high-growth potential.

14. Initial Public Offerings

IPOs allow the NRIs to get in on the ground floor of promising companies. Speaking of the merits of the Initial Public Offerings, they are listed below;

- Early Access: Invest in the companies before they hit the secondary market.

- Growth Potential: There is a possibility of higher returns as the companies grow and establish themselves.

- Diversification: Add variety to your portfolio with different industries.

IPOs are an exciting opportunity for NRIs to tap into the evolving corporate landscape of India.

Why is Investing in India A Good Option for NRIs?

Investing in India is indeed a lucrative opportunity for NRIs, owing to the robust economic growth of the country and the diverse investment options it offers. With one of the fastest-growing economies globally, India presents a range of opportunities across sectors like real estate, mutual funds, equity, and gold, catering to every risk appetite.

Favourable exchange rates provide an added advantage, that in turn allows the NRIs to maximise returns on investments made in Indian Rupees. Additionally, government initiatives like tax benefits on NPS and ULIPs, along with streamlined repatriation processes, make the investment landscape even more appealing and accessible.

Apart from financial benefits, investing in India enables NRIs to maintain a connection with their homeland while being an active contributor to its progress. India has a well-regulated financial ecosystem, which is fueled by institutions like the RBI and SEBI, ensuring transparency and security.

You might be looking for long-term security for your wealth, or exploring high-growth markets. Either way, India’s dynamic economy offers the perfect mix of stability, opportunity, and emotional fulfilment.

Eligibility Criteria for NRIs to Invest in India

Non-Resident Indians (NRIs) have the privilege of investing in a wide array of financial instruments in India, but they must meet the specific eligibility criteria and follow the regulatory guidelines. Here’s a concise overview;

- NRE and NRO Accounts

NRIs must hold either a Non-Resident External (NRE) account or a Non-Resident Ordinary (NRO) account with an authorised Indian bank. These accounts facilitate investments in various financial instruments and manage income earned in India.

- Compliance with FEMA Guidelines

Investments by NRIs are governed by the Foreign Exchange Management Act (FEMA), which outlines permissible investment avenues and restrictions. NRIs must ensure their transactions comply with these regulations.

- Pan Card Requirement

A Permanent Account Number (PAN) card is mandatory for NRIs to invest in India. It is essential for tax reporting and financial transactions like mutual funds, stocks, or real estate purchases.

- Investment Avenues

NRIs are eligible to invest in:

- Mutual funds through NRE/NRO accounts.

- Real estate (excluding agricultural land, plantations, and farmhouses).

- Government schemes like NPS (National Pension System) and ULIPs.

- Direct equity investments and IPOs via Portfolio Investment Schemes (PIS).

- Repatriation Guidelines

Funds invested through NRE accounts are fully repatriable, whereas investments made through NRO accounts have certain limits on repatriation. It’s essential to maintain clear records for seamless fund transfers.

By fulfilling these eligibility criteria, NRIs can access the immense potential of India’s financial market and diversify their investment portfolios effectively.

Why Pentad Securities?

Pentad Securities, Online Share Trading and Investment Broker in India, is a trusted partner for NRIs looking to navigate the complexities of investing in India. With a deep understanding of the Indian financial landscape and years of expertise, Pentad Securities provides personalised solutions tailored to meet the unique goals and aspirations of NRIs. Whether you aim to build long-term wealth, secure your family’s future, or diversify your portfolio, Pentad Securities, your reliable financial partner, offers a seamless and efficient investment experience.

What sets Pentad Securities apart is its commitment to client-centric service, ensuring transparency, credibility, and expert guidance at every step. From assisting with compliance requirements to curating tax-efficient investment plans, Pentad ensures your journey is hassle-free and rewarding. Partner with Pentad to transform your investment aspirations into a prosperous reality, backed by a team that truly understands your needs.

Mutual funds have revolutionised the way individuals approach investing by offering a simple yet effective solution for diversification and risk management. They provide everyday investors access to professionally managed portfolios that were once reserved for institutional players. Mutual funds are highly sought after for their flexibility, offering investors the ease of buying or selling shares with minimal hassle due to strong liquidity and demand. However, one crucial decision investors face is choosing between direct and regular mutual funds. Let’s explore direct vs. regular mutual fund options further to assist you in making a smart selection.

1. What Are Mutual Funds?

Mutual funds are investment vehicles that pool money from multiple investors to buy a diversified portfolio of securities such as stocks, bonds, and other assets. These funds are managed by professional fund managers who make strategic investment decisions based on the fund’s objectives. This allows investors, regardless of their experience, to benefit from professional expertise and access to markets that might otherwise be out of reach.

Types of Mutual Funds

Mutual funds cater to a wide range of financial goals and risk appetites, offering different types to suit investor needs:

- Equity Mutual Funds: These funds primarily invest in stocks, aiming for long-term capital appreciation.

- Debt Mutual Funds: Focused on fixed-income securities like bonds and government securities, these funds provide stable returns with relatively lower risk.

- Hybrid Mutual Funds: Offering a blend of equity and debt, these funds balance growth and stability, making them ideal for moderate-risk investors.

- Sector Funds: Targeting specific sectors like technology, healthcare, or infrastructure, these funds allow for focused investments.

- Index Funds: These funds aim to replicate the performance of a specific market index, such as the NIFTY 50 or Sensex, by investing in the same securities in the same proportion as the index.

By offering this variety, mutual funds ensure there’s something for every type of investor, from risk-averse savers to growth-focused strategists.

How Mutual Funds Work

Fundamentally, mutual funds operate on the principle of pooling resources. When investors contribute money to a mutual fund, the collected corpus is used to purchase a range of securities that align with the fund’s investment strategy. A professional fund manager oversees this portfolio, aiming to maximise returns while managing risks.

The performance of a mutual fund is directly linked to the underlying assets, such as stocks or bonds. This dynamic enables investors to indirectly hold a stake in a variety of instruments, enhancing diversification.

Net Asset Value (NAV):

NAV plays a critical role in mutual fund investments. It represents the per-unit value of a fund and is calculated as:

Net Asset Value Per Share (NAVPS) = (Total Assets – Total Liabilities)/Number of Units Outstanding

NAV fluctuates daily based on market movements and the value of the underlying securities. When investors buy or sell mutual fund units, the NAV determines the price. Understanding NAV is essential for tracking a fund’s performance and making informed investment decisions.

By simplifying complex investment processes, mutual funds empower individuals to participate in markets and grow their wealth systematically.

2. Understanding Direct Mutual Funds

Direct mutual funds represent a streamlined approach to investing, where investors purchase units directly from the Asset Management Company (AMC) without involving intermediaries like brokers or distributors. This bypasses the need for commissions or advisory fees, making direct mutual funds a cost-efficient alternative to regular mutual funds. By dealing directly with the AMC, investors gain greater control over their investment decisions, ensuring a transparent and straightforward process.

How to Invest in Direct Mutual Funds

Investing in direct mutual funds is simple and can be done through multiple channels:

- Directly via AMCs: Visit the AMC’s branch office or website to purchase units without intermediaries.

- Online Investment Platforms: Leverage platforms dedicated to mutual funds that offer direct schemes. These tools often provide comparisons, making it easier to select suitable funds.

- Mobile Applications and Portals: Several apps and portals facilitate the purchase of direct mutual funds, allowing seamless transactions and portfolio management from anywhere.

By utilising these methods, investors can efficiently invest and monitor their portfolios without relying on third parties.

Advantages of Direct Mutual Funds

Direct mutual funds offer a host of benefits that make them attractive, especially for cost-conscious and informed investors:

- Lower Expense Ratio:

One of the standout advantages of direct mutual funds is their reduced cost structure. Since there are no intermediaries involved, AMCs save on distribution fees and pass on these savings to investors, resulting in lower expense ratios compared to regular mutual funds. - Higher Returns:

The absence of distributor commissions allows direct mutual funds to deliver higher returns over time. These cost savings, when compounded, can significantly enhance the overall investment value in the long term. - Control Over Investment Choices:

Direct mutual fund investors enjoy greater transparency and access to fund details. This direct relationship with the AMC ensures that investors can independently evaluate the fund manager’s portfolio and strategies, enabling more informed decision-making.

With these compelling benefits, direct mutual funds have emerged as a preferred choice for savvy investors who prioritise cost-efficiency and autonomy in their financial journey.

3. Understanding Regular Mutual Funds

Regular mutual funds are investment schemes purchased through intermediaries like brokers, distributors, or financial advisors. These intermediaries charge a commission or fee for their services, which is embedded in the fund’s expense ratio. By involving professionals, regular mutual funds cater to investors who seek expert guidance and hands-on support for managing their investments. This approach is particularly beneficial for those new to investing or individuals who prefer a more guided experience.

How to Invest in Regular Mutual Funds

Investing in regular mutual funds is straightforward and accessible through multiple channels:

- Financial Advisors or Brokers: Professional advisors recommend suitable mutual fund schemes based on an investor’s financial goals, risk tolerance, and investment horizon.

- Banks: Many banks act as intermediaries, offering a wide range of mutual fund options for their customers.

- Online Platforms: Digital portals and apps simplify the process of investing in regular mutual funds by connecting investors with financial advisors or brokers for guidance.

These channels provide investors with a convenient and comprehensive approach to entering the mutual fund market backed by professional expertise.

Advantages of Regular Mutual Funds

Regular mutual funds offer several benefits that make them an attractive choice for investors seeking guidance and convenience:

- Professional Guidance:

Investors can rely on financial advisors or brokers to analyse market trends, evaluate fund performance, and recommend investment options that align with their financial goals. This expert advice helps mitigate risks and enhances decision-making. - Convenience:

Brokers and advisors handle the end-to-end process of investing, from completing paperwork to resolving queries. This hassle-free approach allows investors to focus on their financial objectives without getting bogged down by administrative tasks. - Personalised Services:

Regular mutual funds often come with tailored strategies crafted by financial advisors to meet specific goals, such as wealth accumulation, retirement planning, or tax-saving investments. Advisors also periodically review and adjust portfolios to adapt to changing market conditions or client needs.

By offering expert support and a hands-off experience, regular mutual funds are ideal for individuals seeking personalised attention and simplified investment management.

4. Key Differences Between Direct and Regular Mutual Funds

| Key Aspects | Direct Mutual Funds | Regular Mutual Funds |

| Cost Structure (Expense Ratio) | Because there are no commissions to pay to brokers or distributors, the typical expense ratio is low. | Higher expense ratio due to commissions or fees paid to brokers, distributors, or financial advisors |

| Returns on Investment | Higher returns over time, as the absence of commission fees means more of your investment’s returns go directly to you. | Slightly lower returns because of the additional commissions, reducing the overall returns on investment. |

| Investment Process | Direct interaction with the Asset Management Company (AMC), usually done online, offers a quicker, more streamlined process. | Requires intermediaries such as brokers, financial advisors, or banks, which can involve additional paperwork and steps. |

| Suitability | Best suited for experienced or self-directed investors who are comfortable researching, selecting, and managing their investments. | Ideal for new investors or those seeking professional assistance to make informed decisions about their investments. |

| Transparency | Full transparency about the fund’s performance and expenses, as no middlemen are involved. | Transparency can be limited, as intermediaries might withhold certain details, leaving investors without a full understanding of the process. |

| Availability of Advice | No advisory support; investors must rely on their own knowledge or research. | Includes advisory support, which may help in making informed investment decisions. |

5. Who Should Choose Direct Mutual Funds?

Direct mutual funds are tailored for specific types of investors who value autonomy, cost-efficiency, and long-term growth. Here’s a breakdown of who benefits the most from this investment option:

- Self-Directed Investors

Investors with the expertise to independently evaluate mutual funds are ideal candidates for direct mutual funds. These individuals possess the knowledge to assess fund performance, market trends, and investment goals without relying on brokers or advisors. By bypassing intermediaries, they retain full control over their investment decisions.

- Long-Term Investors

Direct mutual funds are a natural choice for those with a long-term investment horizon. The absence of intermediary fees results in a lower expense ratio, allowing more returns to compound over time. This makes direct funds particularly appealing for individuals focused on wealth creation over decades.

- Tech-Savvy Individuals

In the digital age, managing investments online has become seamless. Tech-savvy investors who are comfortable navigating websites, apps, and online platforms can easily access direct mutual funds. The convenience of comparing funds, using tools, and tracking performance online empowers these investors to make informed decisions.

- Cost-Conscious Investors

Direct mutual funds cater to those who prioritise keeping costs low. With no commissions paid to brokers or advisors, the expense ratio is significantly reduced, ensuring that more returns go directly to the investor. Cost-conscious individuals who value efficiency in financial planning find this option particularly rewarding.

Choosing direct mutual funds is all about aligning investment strategies with personal preferences and financial goals. For those ready to take charge of their investments, these funds offer a blend of control, transparency, and cost savings.

6. Who Should Choose Regular Mutual Funds?

Regular mutual funds are an excellent option for investors who value expert guidance and convenience in managing their investments. Here’s a closer look at who benefits most from choosing this approach:

- New or Inexperienced Investors

For those who are new to the world of mutual funds, the investing landscape can seem complex and overwhelming. Regular mutual funds provide the advantage of working with experienced brokers or financial advisors who can simplify the process. These professionals guide investors in selecting funds that align with their financial goals and risk tolerance, making it an ideal choice for beginners.

- Investors Seeking Personalised Guidance

Some investors prefer a hands-on approach from financial experts. Regular mutual funds offer tailored advice on portfolio allocation, fund selection, and ongoing investment strategies. Advisors consider the investor’s unique financial situation and long-term objectives to design a customised plan that suits their needs.

- Time-Starved Investors

For individuals who have busy schedules or lack the inclination to actively manage their investments, regular mutual funds provide a hassle-free solution. Advisors and brokers handle the legwork, from researching funds to completing paperwork and addressing queries. This makes it easier for investors to stay on track without dedicating significant time to the process.

- People Seeking Risk Mitigation

Risk management is a crucial aspect of successful investing, especially for those new to the market. Regular mutual funds offer professional expertise in evaluating an investor’s risk profile and recommending funds that strike the right balance between risk and returns. This guidance helps beginners avoid common pitfalls and build a diversified portfolio aligned with their financial goals.

Opting for regular mutual funds is a smart choice for investors who prefer expert support and the convenience of having professionals manage their investments. By leveraging the knowledge and resources of financial advisors, investors can navigate the complexities of mutual fund investing with confidence.

7. Cost Comparison: Direct vs Regular Mutual Funds

When deciding between direct and regular mutual funds, the cost structure plays a crucial role. Here’s a detailed comparison to highlight the differences:

Expense Ratio Breakdown

The expense ratio is a measure of the annual cost required to operate and manage an investment fund, represented as a percentage of the fund’s total average assets. It covers management fees, administrative costs, and, in the case of regular mutual funds, distributor commissions.

- Direct Mutual Funds: Typically have a lower expense ratio because they do not include distributor commissions.

- Regular Mutual Funds: Have higher expense ratios due to intermediary fees.

Example:

Let’s assume an initial investment of ₹1,00,000 with a return of 12% per annum:

- Direct Fund: Expense ratio of 1.0%

- Regular Fund: Expense ratio of 1.5%

Formula for Future Value (FV):

FV = PV(1 + r)^n

PV = Present Value

r = Interest rate per period (after deducting expense ratio)

n = Number of periods

Here,

PV = ₹1,00,000

For direct funds, net growth rate r = 12% – 1% = 11% (0.11)

For regular funds, net growth rate r = 12% – 1.5% = 10.5% (0.105)

Calculation of Impact Over Time:

| Year (n) | Direct Fund (₹) | Regular Fund (₹) | Difference (₹) |

| 5 | 1,68,506 | 1,64,745 | 3,761 |

| 10 | 2,83,942 | 2,71,408 | 12,534 |

| 20 | 8,06,231 | 7,36,623 | 69,608 |

Key Observations:

- Over 20 years, a 0.5% higher expense ratio reduces returns by nearly ₹69,608.

- The gap grows exponentially due to the power of compounding.

Impact of Higher Fees on Compounded Growth

Small differences in fees might seem negligible in the short term, but over time, they compound and can substantially reduce wealth.

- Direct Mutual Funds: By minimising costs, they allow investors to retain a larger portion of their returns, which further compounds over time.

- Regular Mutual Funds: Higher fees erode returns, leading to a noticeable gap in accumulated wealth, particularly for long-term investments.

Example:

Imagine investing ₹10 lakh over 20 years with the same annual return (12%) and the same expense ratio:

Direct Fund Growth:

- Net growth rate = 11% (0.11)

- After 20 years:

FV = 10,00,000 × (1 + 0.11)^20 = 80,62,312

Regular Fund Growth:

- Net growth rate = 10.5% (0.105)

- After 20 years:

FV = 10,00,000 × (1 + 0.105)^20 = 73,66,235

Wealth Loss Due to Fees:

- Difference = ₹80,62,312 – ₹73,66,235 = ₹6,96,077

Over a period of 20 years, the impact of higher fees in regular mutual funds can lead to a loss of nearly ₹6.96 lakh on an investment of ₹10 lakh. This substantial difference arises due to compounding, where even small variations in expense ratios accumulate into significant wealth erosion over time. The impact underscores why cost-conscious investors, especially those with long-term horizons, often prefer direct mutual funds. By keeping expenses low, they unlock the full potential of compounding to grow their wealth effectively.

Choosing between direct and regular mutual funds requires careful consideration of how costs will impact your financial goals. Understanding the long-term implications of expense ratios can help you make an informed decision and maximise your investment returns.

8. How to Choose Between Direct and Regular Mutual Funds?

Choosing the right type of mutual fund—direct or regular—depends on your financial needs, investment experience, and priorities. Here’s a step-by-step guide to support you make a well-informed choice:

i) Evaluate Your Investment Knowledge

Before choosing a fund type, assess your expertise:

- Do you have a good understanding of mutual funds, market trends, and portfolio management?

- Are you confident in selecting funds based on performance, asset allocation, and expense ratios?

If yes, direct mutual funds might be the right choice, as they empower knowledgeable investors to take full control. If not, you may benefit from the professional guidance offered with regular funds.

ii) Consider Your Financial Goals and Risk Tolerance

- Define your financial objectives: Are you saving for retirement, a child’s education, or a short-term goal?

- Assess your risk appetite: Are you comfortable with market fluctuations, or do you prefer safer options?

Direct funds suit those with clear goals and a good grasp of investment risks. Regular funds, guided by advisors, help align investment choices with both short- and long-term goals while managing risk effectively.

iii) Look at the Role of a Financial Advisor

- Are you confident in making investment decisions without assistance, or do you require expert input?

A financial advisor can analyse your financial situation, recommend suitable funds, and offer insights into rebalancing and diversification. This service, integral to regular funds, is especially valuable for beginners or busy investors.

iv) Assess Convenience vs. Cost

- Are you willing to pay slightly higher fees for the convenience of professional assistance?

- Would you prefer lower costs and take on the responsibility of managing your investments independently?

If you prioritise cost efficiency and are ready to put in the effort to research and monitor investments, direct funds are ideal. On the other hand, regular funds offer time-saving convenience and expert guidance for those who value professional support.

Choosing between direct and regular mutual funds ultimately hinges on your investment knowledge, goals, and priorities. Direct funds are cost-effective and suitable for self-driven investors, while regular funds offer personalised advice and ease for those new to the investment landscape. Carefully evaluate your needs and resources to decide which option best aligns with your financial journey.

9. Common Mistakes to Avoid When Choosing Mutual Funds

Investing in mutual funds can be an excellent way to grow wealth, but avoiding common mistakes is crucial to maximising returns and achieving financial goals. Here are the pitfalls you should steer clear of:

- Not Comparing Expense Ratios

The expense ratio significantly impacts your returns, especially over the long term. Many investors overlook this critical factor and end up paying higher fees unnecessarily. A fund with a high expense ratio reduces your net returns. For instance, a 0.5% difference in expense ratios could mean losing thousands over a decade. Always compare the expense ratios of similar funds before making your choice. Opt for funds with lower expense ratios to maximise your earnings.

- Choosing Funds Based Only on Past Performance

Historical performance is often a go-to metric for investors, but relying exclusively on it can be misleading. Past success doesn’t guarantee future results as market conditions and fund strategies evolve. A fund that performed well in the past may struggle in different market environments. Look beyond past performance by evaluating the fund manager’s expertise, current portfolio composition, and alignment with your investment goals.

- Overlooking Asset Allocation

A mutual fund might look great on its own, but ignoring how it fits into your overall portfolio can lead to imbalances. Poor asset allocation can increase risk or limit growth. For example, over-investing in equity funds might expose you to unnecessary market volatility. Ensure your fund choices complement your overall asset mix and align with your risk tolerance and investment horizon.

- Ignoring the Need for Professional Advice

Many investors underestimate the value of expert guidance, either overestimating their knowledge or hesitating to pay for professional services. Decide between direct and regular mutual funds with careful consideration. Choosing direct funds without adequate research or expertise can result in poor investment decisions. Conversely, paying for regular funds unnecessarily when you can manage investments independently adds avoidable costs. Assess your expertise and willingness to manage your investments. Seek professional advice if you’re unsure, but if you’re confident and knowledgeable, direct funds might be a better choice.

Conclusion

Choosing between direct and regular mutual funds depends on your investment style, goals, and level of expertise. Direct mutual funds offer the advantage of lower expense ratios and higher potential returns, making them ideal for cost-conscious and self-directed investors. However, they require a deeper understanding of the market and active management. On the other hand, regular mutual funds provide professional guidance and convenience, making them suitable for beginners or those with limited time to manage their portfolios, albeit at a higher cost due to distributor commissions.

Why Choose Pentad Securities?

Navigating the complexities of mutual fund investments requires a reliable partner, and Pentad Securities, an Online Share Trading and Investment Broker in India, stands out as an excellent choice. Our customised and goal-oriented advisory support ensures your investments align with your financial aspirations while regular monitoring and assessment keep your portfolio on track. We provide a diverse range of financial products tailored to suit every investor’s needs. With expert guidance and real-time insights, Pentad helps both new and experienced investors navigate market fluctuations confidently and maximise returns. Whether you prefer direct or regular funds, Pentad provides the tools and strategies to achieve your investment goals.

Investing wisely is essential for financial growth and Systematic Investment Plans (SIPs) have emerged as one of the most popular and efficient ways to build wealth over time. SIPs offer a disciplined approach to investing, enabling individuals to contribute regularly to their preferred mutual funds while benefiting from market fluctuations and the power of compounding.

This blog will give you a clear idea about everything you have to know about SIPs, including their benefits and how they work.

You may also like to read:

- How Can NRIs Invest in Indian Mutual Funds – Complete Guide

- How to Invest in Silver in India – Smart Ideas from Pentad

- A Comprehensive Guide to Gold Hedging: Protecting Your Investments

What Is an SIP?

A Systematic Investment Plan (SIP) is a structured way to invest in mutual funds, allowing individuals to regularly invest a fixed amount in a scheme of their choice.

This investment plan focuses on gradually investing smaller sums over time instead of making a single large investment, ultimately leading to potentially higher returns.

How SIP Works?

The process of investing through SIP involves a few straightforward steps. This includes:

1. Auto debit from Your Bank Account: If you sign up for a SIP, you authorise the bank to auto-debit a specific sum of money at regular intervals (monthly, quarterly, etc.). This amount is then invested in the mutual fund scheme of your choice.

2. Purchase of Units of Mutual Funds at Prevailing Market Rates: The amount debited from the account is used to purchase mutual fund units at the market rate of the date of investment. The number of units you get depends on the fund’s current Net Asset Value (NAV).

3. Impact of Rupee Cost Averaging: Over time, as you continue investing regularly through SIPs, you benefit from rupee cost averaging. This means that when the market price of a mutual fund goes down, you purchase more units and when the prices are high, you buy fewer units. This strategy helps reduce the average cost of your investment over time.

Key Benefits of SIP Investments

Systematic Investment Plans (SIPs) are a popular investment option for those who wish to grow their wealth in a structured and disciplined manner. This is a great choice for both investors and beginners considering its flexibility, affordability and the potential for significant returns. Here are some of the key benefits of SIP investments.

- Rupee Cost Averaging

One of the standard advantages of SIP investments is rupee cost averaging. This concept means you invest a fixed amount at regular intervals, regardless of marketing conditions. When the markets are low, your fixed amount buys more units; when the markets are high, you purchase fewer units. This evens out the average cost of your investments over time, making market instability less of a problem.

This approach is ideal for those who are wary of timing the market but want consistent growth for their portfolio.

- Discipline and Regularity

SIP investments instil a sense of financial discipline by encouraging regular contributions to your investment portfolio. By automating your investments, you are less likely to miss payments or get distracted by impulsive spending habits. This disciplined approach is the best way to help you build wealth over time but also ensure you stay committed to your long-term financial goals.

- Compounding Benefits

SIPs leverage the power of compounding to maximise your returns. When you reinvest the earnings generated from your investments, they start earning returns as well. Over time, this cycle of earning and reinvesting leads to exponential growth.

For example, starting early with even a modest SIP can result in significant wealth accumulation with a compounding effect.

- Lower Risk for New Investors

For those who are new to investing, stock marketing can seem intimidating and SIPs are a safer entry point. This allows you to invest small amounts gradually rather than making a large lump-sum investment. This helps you avoid the risk of significant losses and makes it easier to manage emotions during market fluctuations. Moreover, SIPs diversify your investments over time, further minimising the risks associated with market volatility.

- Affordability

SIPs are incredibly affordable, making them accessible to a wide range of investors. The affordability feature of DIPs makes it an excellent choice for young professionals, students, or anyone looking to start investing without financial strain.

Types of SIPs

Here are different types of SIPs

| Type of SIP | Description | Benefits |

| Top up SIP | Allows you to increase the SIP amount at regular intervals. | It helps align your investments with income growth and achieve financial goals faster. |

| Flexible SIP | It lets you adjust the SIP amount or skip payment based on your financial situation. | Provides flexibility to manage investments during unforeseen expenses or income fluctuations. |

| Perpetual SIP | It has no fixed end date and it continues until you decide to stop it or withdraw funds. | Suitable for long-term goals, offering consistent investments without setting specific timelines. |

Read more about:

- 11 Child Investment Plans in 2025: Investing for Your Child’s Future – Guide

- Halal Investing: Balancing Financial Growth with Ethical Values

- Risk Management in Derivative Trading: Strategies and Techniques

How to Choose the Right Mutual Fund for SIP

Choosing the appropriate mutual fund for your Systematic Investment Plan (SIP) is essential for achieving your financial goals. With countless funds available, finding the one that matches your preferences can be challenging. Here are some key factors to consider when choosing the perfect mutual fund for your SIP investment.

Risk Profile Assessment

Investing in mutual funds requires an understanding of your personal risk tolerance. This ranges from low to high, depending on your financial situation and investment goals.

- Understanding Your Risk Tolerance:

Risk tolerance is your ability and willingness to take risks. This can be categorised into:

Low Risk: Suitable for conservative investors seeking stable returns. Debt funds or liquid funds are ideal for this profile.

Medium Risk: It is suitable for moderate investors who prefer a balance of risk and reward. Hybrid funds are a good option here.

High Risk: Ideal for aggressive investors seeking higher returns and willing to tolerate the fluctuations in the market. Equity funds are often preferred in this category.

- Matching Risk with Fund Types:

After determining your risk tolerance, choose a fund that aligns with it. For instance, stock funds may provide higher returns but are more volatile, whereas debt funds are more reliable but produce lower returns.

Investment Horizon

Your investment duration plays a significant role in selecting the right mutual fund.

- Short-Term Goals

If you are planning to invest for 1 to 3 years, it is better to choose funds with lower risk, such as debt funds, liquid funds or ultra-short-term funds. These options provide stability and liquidity.

- Long-Term Goals

For goals extending beyond 5 years, equity funds or index funds are a better choice due to their potential for higher returns over time. These funds benefit significantly from market growth and the power of compounding.

Fund Performance & History

Evaluating a fund’s historical performance is critical to making an informed decision.

- Historical Performance:

Check how the fund has performed over the past 3, 5 and 10 years. Instead of focusing just on exceptional short-term results, look for regular returns. This demonstrates the fund’s capacity to perform over multiple market cycles.

- Fund Managers:

The expertise and experience of fund managers play a key role in delivering returns. Research their track record and how they have managed similar funds in the past.

Explanation of Expense Ratio:

It is expressed as a percentage of your investment. For instance, if a fund has an expense ratio of 1.5%, ₹1.50 is deducted annually for every ₹100 invested.

- Impact on Returns:

A higher expense ratio can reduce returns over time, especially in long-term investments. Compare the expense ratios of funds within the same category to identify cost-effective options.

How to Start an SIP Investment?

| Step | Details |

| Choose a Mutual Fund | Research and select a mutual fund that aligns perfectly with your financial goals and risk profile. |

| You can invest directly through the fund house’s website or via an investment platform or app for convenience. | |

| Select the SIP Amount and Frequency | Decide how much you like to invest (e.g.,₹500, ₹1,000, etc.). |

| Choose the frequency of investment: monthly, quarterly or annually. | |

| Complete the KYC (Know Your Customer) Process | KYC is mandatory for mutual fund investments. You need to provide personal details, including a PAN card and address proof. |

| Complete the process online via e-KYC or offline by visiting the nearest fund office. | |

| Platforms and Apps for SIP Investments | Use online platforms or mutual fund investment apps to simplify the process. |

| Decide between Direct (no intermediaries, lower expense ratio) and Regular (through a broker/advisor, slightly higher fees) plans. | |

| Documents Required for KYC and SIP Setup | PAN card |

| Address proof (e.g., Aadhaar card, utility bill) | |

| Bank account details (cancelled cheque or passbook copy) | |

| Ensure that your email ID and mobile numbers are registered for communication and OTP verifications. |

Factors to Consider Before Starting an SIP

SIPs are one of the best ways to achieve financial goals and before starting this journey, it’s essential to evaluate several factors to ensure your investment strategy is effective and aligned with your needs. The following are some of the key considerations to make an informed decision.

- Liquidity Needs

- Short-Term Financial Needs:

Before beginning to invest in SIPs, assess whether you might need the invested money in the short term. These are better suited for medium to long-term financial goals, as withdrawing funds prematurely could hinder your overall returns.

- Redemption Processes and Timelines:

Different mutual funds have different redemption procedures and timelines. For instance, equity funds may take a few days for redemption, while liquid funds offer faster withdrawal options. Evaluate the liquidity options of your chosen fund to avoid inconvenience.

- Market Volatility

- Impact of Market Fluctuations

SIPs are designed to navigate market volatility by leveraging rupee cost averaging. This strategy helps mitigate the impact of market highs and lows by spreading your investments over time.

- Adopting a Long-Term Perspective

While market fluctuations are inevitable, a long-term investment horizon allows you to ride out short-term volatility and achieve stable returns.

Monitoring and Reviewing Your SIP

Starting an SIP is not a one-time decision. It requires continuous monitoring and reviewing, which is crucial as it is aligned with your financial goals and marketing conditions. The different ways to manage SIP investments are:

Performance Review

- Tracking your SIP Performance:

Assess your SIP’s performance regularly using online tools or review the fund’s NAV (Net Asset Value) and compare its returns with benchmark index and peer funds to ensure consistency.

- Annual Portfolio Reviews:

Conduct a detailed portfolio review at least once a year to evaluate whether your SIP investments are delivering the expected results. This is also the time to check whether the strategies of the fund manager align with your objective.

- Rebalancing Your Portfolio:

If certain funds underperform or market dynamics shift, consider rebalancing your portfolio by relocating your investments to better-performing funds.

When to Stop or Modify an SIP

- Reassuring Goals:

Life circumstances and financial goals may change over time. If your SIP is no longer in alignment with your needs, you might consider stopping or modifying it.

- Increasing SIP Amounts:

When your income grows, consider increasing your SIP contributions to accelerate wealth growth. Most platforms are offering top-up SIP options to automate this process.

- Switching Funds:

If your chosen fund consistently underperforms or no longer suits your risk profile, it is better to switch to a more suitable mutual fund.

Impact of Market Conditions

- Understanding Market Impact on SIP Performance:

Market downturns may temporarily affect SIP returns. But this doesn’t mean you should panic. Staying invested when the market is down can often lead to better returns when the market recovers.

- Avoid Emotional Decisions:

SIPs are long-term investments designed to weather market volatility. Avoid stopping or withdrawing your SIP during market dips as this could lock in losses and hinder your financial goals.

Common SIP Investment Mistakes to Avoid

SIPs or Systematic Investment Plans are a reliable and disciplined way to invest. However, many investors need to be aware of mistakes that can impact their returns. Avoid these mistakes to ensure this SIP journey is smooth and aligned with your financial goals.

Chasing High Returns

- Dangers of Timing the Market:

One of the biggest mistakes is attempting to time the market to achieve higher returns. SIPs are designed to mitigate volatility through rupee cost averaging but chasing unrealistic returns can lead to impulsive investment decisions.

- Focus on Consistency Over Returns:

Try to prioritise consistent investment in funds rather than targeting high returns that align with your risk profile and financial objectives. Note that SIPs are more effective when approached from a long-term perspective.

Not Reviewing Your SIP Regularly

- Importance of Performance Checks:

Many investors set up SIPs and forget about them. This can be risky as market dynamics and fund performance can change over time. Regularly reviewing your SIP ensures it aligns with your financial goals and continues to deliver expected returns.

- Adjusting When Necessary:

During your reviews, consider rebalancing your portfolio if a fund consistently underperforms or if your financial goals change.

Investing Without a Financial Goal

- The Role of Clear Goals:

SIPs are most effective when tied to specific goals, such as retirement, buying a house, or funding a child’s education. Without a clear goal, choosing the right mutual fund can be challenging.

- Set Measurable Objectives:

Before starting as SIP, set specific, measurable, and time-bound goals.

SIP for Financial Goals

SIPs are versatile investment tools that can help you achieve various financial goals. Here are some SIPs that can cater to your different financial goals.

- SIP for Retirement Planning

Retirement is a long-term financial goal, which makes SIP an ideal choice. It can benefit from compounding and rupee cost averaging over an extended period.

If you have a long-term retirement goal, equity funds are often the best option thanks to their higher growth potential over time.

- SIP for Child’s Education/Marriage

Education and marriage are two significant milestones that require considerable financial planning. SIP is a great choice as it allows you to start early and gradually build a corpus without financial strain.

For medium goals, consider hybrid or balanced funds, which offer a mix of stability, growth, and reduced overall risk.

- SIP for Wealth Creation

Consistent investing over the long term allows you to benefit from the power of compounding. SIPs make wealth creation accessible even with small initial investments.

These funds provide exposure to multiple sectors and industries, which reduces the risk and enhances growth potential.

Conclusion

SIP investments are an accessible and effective pathway for individuals to navigate through various types of investments. The process of SIPs is quite simple and manageable, opening up opportunities for investors across the financial spectrum. Whether you are new to investing or experienced, understanding various types of SIPs can empower you to select the investment strategy that can meet your specific goals and adapt to changing financial circumstances.

Pentad Securities, an Online Share Trading and Investment Broker in India, is dedicated to enhancing investor knowledge about the different financial plans available and guiding them in choosing the most suitable investment options, plans, and solutions adapting to their financial abilities.

We offer a range of investment strategies designed to cater to both experienced and new investors. Our goal is to help you find solutions that offer a good balance of safety, returns, and growth potential. Contact us today to discover our investment opportunities or to schedule a consultation to discuss your financial objectives.

India’s Mutual Fund market isn’t just growing—it’s becoming a powerhouse of investment opportunities. Mutual funds are a great avenue for Non-Resident Indians (NRIs) to diversify their portfolio, and generate wealth, while also staying connected to India’s economic growth story. However, the legal and regulatory requirements make the process daunting for so many.

In this guide, we break down the investment process step by step from the basics, tax implications, and practical tips to make it smooth sailing.

You may also like to read:

- How NRIs Can Invest in Indian Stock Market: A Complete Guide

- How to Invest in Silver in India – Smart Ideas from Pentad

- How to Invest in Sovereign Gold Bond

Why Mutual Funds are a Good Choice for NRIs?

Mutual funds are investment portfolios that pool money from various investors, to invest in the stock, bonds, or any other securities. For NRIs, mutual funds offer several benefits:

- Ease of Access: Thanks to modern digital platforms, people can invest and manage their portfolios irrespective of their location.

- Diverse Options: From equity to debts, and hybrid funds, investors can use mutual funds to build wealth, reduce risks, or look for regular income.

- Professional Management: The fund managers consistently monitor the market to optimise returns, taking the burden away from investors

The mutual fund market in India stood at over ₹46 trillion in 2023 and had a CAGR of 17% over the past decade. Using mutual funds, NRIs have been able to invest in some of the country’s high-growth sectors, such as Information Technology, pharmaceuticals, and infrastructure—areas that have been some of the major growth drivers.

Eligibility Criteria for NRIs to Invest in Mutual Funds

To invest in mutual funds in India, NRIs are required to meet certain essential criteria. According to FEMA, an NRI is an Indian citizen who has been living in another country for employment, business, vocational or any other activities or for any other purpose in that country and has continued to be an Indian citizen; or is registered as an overseas citizen of India.

Requirements for Investment:

- PAN Card: It is compulsory to have a PAN, or Permanent Account Number, for any financial transaction in India.

- KYC Compliance: Know Your Customer (KYC) process involves all investors including the NRIs providing identification, address proof and a FATCA self-certification.

- Bank Accounts: Anyone interested in investing has to open an NRE (Non-Resident External) or an NRO (Non-Resident Ordinary) account.

Types of Investment Accounts

NRIs can use either of the following accounts, based on their repatriation needs:

NRE Accounts:

- Ideal for funds that need to be repatriated to the investor’s country of domicile.

- Tax-free principal and interest in India

NRO Accounts:

- Suitable for managing income earned within India like rental income or dividends.

- The developed funds are non-repatriable beyond a certain extent, and the interest formed therein is also taxable.

Modes of Investment

NRIs can invest in mutual funds through:

- Direct Investment:

- It is very easy to invest directly through online portals or the website of the concerned AMC.

- There are AMCs out there that offer video-based KYC making it easy to onboard customers.

- Authorised Distributors:

Distributors are intermediaries and in most instances, they offer other related services.

- Power of Attorney (PoA):

NRIs are allowed to give a Power of Attorney to a local person in India to manage their investment. It gives the PoA holder the ability to conduct transactions provided they meet the KYC checks.

Steps to Start Investing

Here’s a step-by-step guide for NRIs to begin their mutual fund investment journey:

- Open an NRE or NRO Bank Account:

Choose an account depending on whether you need repatriation benefits.

- Complete KYC Formalities:

Photocopy and sign an attested copy of your passport, visa and the address proof where you reside overseas. FATCA compliance is a must for US-based NRIs.

- Select the Right Mutual Fund Scheme:

Make decisions based on your financial objectives, risk tolerance, and the investment period. For example:

- Equity Funds: When you put your money at high risk, targeted for high return.

- Debt Funds: Low-risk, steady income.

- Hybrid Funds: Taking a balanced approach to risk and return.

- Invest and Monitor:

Invest with a large amount of money or with a recurring amount through SIP. With digital platforms, it’s easy to analyse the performance and adjust as needed.

Read more about:

- A Comprehensive Guide to Gold Hedging: Protecting Your Investments

- Halal Investing: Balancing Financial Growth with Ethical Values

- Risk Management in Derivative Trading: Strategies and Techniques

Tax Compliances for Non-Resident Indians

Taxes form a central component of investment in mutual funds by NRIs. Here’s a breakdown:

- Equity Mutual Funds:

- Short-term gains (holding <1 year): Taxed at 20%.

- Long-term gains (holding >1 year): It charged at 10 % of the amount, which is beyond ₹1 lakh.

- Debt Mutual Funds:

- Short-term gains (holding <3 years): Subject to Indian Income Tax at the tax rate applicable under the income tax slab regime.

- Long-term gains (holding >3 years): Imposable to a 20% tax with indexation privileges.

- TDS (Tax Deducted at Source):

- TDS applies to both short-term gains and long-term gains, however, the excess amount can be claimed through tax returns.

Pro Tip: Get advice from a tax consultant to know the prospects of getting rid of double taxation through the Double Taxation Avoidance Agreement (DTAA).

Challenges Faced by NRIs

While mutual funds offer numerous benefits, NRIs may encounter challenges such as:

- Currency Fluctuations:

Fluctuations in exchange rates may make an impact on returns particularly if made on a revenue basis.

- Regulatory Compliance:

In particular, it needs scrupulous compliance with FEMA and FATCA regulations. The good news is that by hiring a professional advisor, the process can be made a lot easier.

- Higher TDS Rates:

NRIs are subjected to higher tax deduction rates than the resident Indians, it will influence short-term liquidity.

- Access to Information:

It becomes challenging to know how our funds are performing, and what the market trends around the globe are. Choose reliable portals, which will provide you the detailed insights.

Relevant Statistics

- More than 60 per cent of NRIs prefer SIPs, valuing the discipline and cost-effectiveness of the approach to investing.

- Hybrid schemes also remain popular; NRIs invest 45% of their total money in equity funds.

Practical Tips for NRIs

- Diversify Globally: Although there is a great opportunity in mutual funds in the Indian market, you should hedge your bets so to speak by investing in funds from other countries.

- Set Clear Goals: Whether you’re investing for retirement, or your child’s education or wealth build-up, define your objectives to choose the right funds.

- Monitor Regularly: Monitor your investment online through apps, or web portals and adjust if necessary

In Conclusion

NRIs have a simple and effective way to invest in India’s economic growth by investing in mutual funds. With the knowledge about its legal requirements, taxation and investment strategies NRIs can deal with it confidently. With adequate planning and support, including mutual funds in your financial portfolio can work wonders for growth and stability.

Seize the moment, and invest in the Indian mutual funds arena. Be it an equity, debt or hybrid fund; every investment choice you make will make you one step closer to your financial goals while keeping in tune with the growth story of India that you are now a part of.

The IMF has projected a 6.5% growth in India’s GDP, thereby making the country a very attractive destination for equity investors. NRIs too are investing in the Indian stock market to gain from the country’s growth.

Basics an NRI Must Know about the Indian Stock Market

There are a number of rules, regulations, and guidelines that every NRI planning to invest in the Indian stock market must be aware of. Moreover, there are very specific procedures that must be carried out. But that should never hold you back as these regulations and procedures are now more accessible than ever.

The following guide shall walk the NRI through the process of commencing investment in the Indian stock market: from the selection of appropriate bank accounts and understanding RBI schemes to comprehending related tax considerations. With the following steps, NRIs will be able to take part in one of the world’s most dynamic markets and fill their portfolio while gaining exposure to India’s growth story.

Read more about:

- FAQ About NRI Mutual Fund Investments – All your Questions Answered

- Risk Management in Derivative Trading: Strategies and Techniques

- How to Invest in Silver in India – Smart Ideas from Pentad

Types of NRI Bank Accounts

In order for the NRIs to invest in the Indian market, they have to open certain bank accounts that would enable them to manage their funds and transactions of investment easily. The following are the bank accounts for NRIs.

- NRE (Non-Resident External) Account: This is a rupee-denominated account opened to extend the facility to NRIs for depositing and managing foreign-sourced income in India. The NRE account gives a full repatriation facility-the principal and interest can be freely repatriated to the country of residence. It’s the preferred account for those aiming to bring overseas earnings into India for investment.

- NRO (Non-Resident Ordinary) Account: The locally earned income in India, such as rent or dividends, is dealt with through the NRO account. Though this is rupee-denominated, there are certain restrictions on repatriation: An NRO account offers up to $1 million per financial year for repatriation, attracting taxes. It’s suited for NRIs who wish to manage both Indian and foreign income in one account.

- FCNR Account: The account is quite useful for those NRIs who prefer maintaining their savings in foreign currency, like the USD or GBP, and thus avoid the associated risks of currency fluctuation. While FCNR accounts are not used to typically invest in the stock market, they work out just perfectly for long-term savings and financial security in foreign currency.

Portfolio Investment Scheme (PIS)

PIS allows investment by NRIs in Indian stocks and mutual funds, which are issued by the Reserve Bank of India. All investment under the scheme of PIS has to be transparent, and everyone must strictly adhere to the rules and regulations laid down by the Indian Government. With every purchase and sale transaction, the authorized bank communicates back to the RBI, bringing compliance and protection for the NRI investor upon opening a PIS account.

How to Invest in the Indian Stock Market by NRIs?

An NRI can depict investment in Indian stock markets by opening a PIS-compliant bank account with a demat account. Through these accounts, NRIs can make direct investments in equities or choose mutual funds. Even websites allow subscriptions to Initial Public Offerings, after which one can buy the shares of companies before those hit the secondary market.

Streamlined processes further allow NRIs to trade shares on the BSE and NSE, thereby developing a portfolio suited to their goals of investment.

Three Ways NRIs Can Invest in Indian Equities

NRIs can invest in Indian equities through the following methods:

- Direct Equity Investment: Under the PIS account, an NRI can directly invest in individual shares listed on Indian Exchanges. By doing so, they can have a diversified stock portfolio. This alternative will work for those who want hands-on investment in particular companies or sectors.

- Investment through Mutual Funds: These are managed funds whose portfolios comprise a mix of equities and bonds. Investment through mutual funds is an easy way for NRIs to invest without the need to select individual stocks. For the investors, the option to choose equity, debt, or hybrid funds based on the risk appetite that best fits makes mutual funds stand out as an attractive diversified exposure.

- Exchange-Traded Funds: Exchange-traded funds combine the features of both stocks and mutual funds, offering liquidity and diversification. For NRIs, ETFs offer diversified, cost-effective investing in a particular index, sector, or commodity with flexibility and lower transaction costs.

You may also like to read:

- 11 Child Investment Plans in 2025: Investing for Your Child’s Future – Guide

- How to Invest in Sovereign Gold Bond

- A Comprehensive Guide to Gold Hedging: Protecting Your Investments

NRIs May Invest on Repatriable or Non-Repatriable Basis

NRIs may invest on either a repatriable or a non-repatriable basis, depending upon their objectives:

- Repatriable Investments: The investments made through its account are fully repatriable, meaning the principal and return are payable abroad. It is a go-to option for those NRIs who seek flexibility in drawing funds out from India internationally.

- Non-Repatriable Investments: The investments through an NRO account are non-repatriable beyond the limit, meaning thereby that such investments stay in India. This is suited for NRIs who plan to keep funds within the country for future needs.

What is PINS Approval from RBI?

Portfolio Investment Scheme (PINS) approval from the RBI is Rs. 10 lakh or $2,500 for NRIs dealing in Indian equities. This gives assurance that the investments by NRIs are tracked and put under scrutiny. Banks report every transaction through PINS to the RBI to show the transparency of transactions and adherence to Indian investment laws. PINS approval enables NRIs to trade confidently in Indian stocks within the ambit of regulatorily acceptable norms.

Documents Required for Opening

Trading cum Demat Account Documents required by an NRI to open a trading and demat account are as follows:

- Identification Proof: Passport, visa, and proof of overseas address.

- PIS Approval Letter: The letter will be issued by the bank in which the PIS account is maintained.

- PAN Card: This is required in paying one’s taxes in India.

- Bank Account Details: NRE or NRO account linked to the PIS account.

These may further be supplemented with additional KYC documents depending upon the demand by the brokers. It is always better to ensure that the NRIs have all the required documents to open the account before proceeding with the process.

How NRIs Actually Undertake the Trading Process

The following is the trading process of NRIs:

- Step 1: Transferring funds to the trading account from the NRE or NRO account.

- Step 2: Trade and investment dealing: chose stock through the trading terminal and issued buy/sell transaction orders to BSE or NSE.